Page 166 - CA Final PARAM Digital Book.

P. 166

also communicated to the management that he plans to include revenue recognition as key audit

matter in his audit report. The management did not agree with revenue recognition to be shown as

key audit matter in the audit report. Comment.

OR

“The auditor shall determine, from the matters communicated with those charged with governance, those

matters that required significant auditor attention in performing the audit. In making this determination,

the auditor shall take into account the key factors”.

You are required to briefly discuss the factors determining the key audit matters.

Answer Part I -- Relevant Standards & Laws

▪ SA 701 – Communicating Key Audit Matters In The Independent Auditor’s Report

Part II -- Requirements of Relevant Standards & Laws

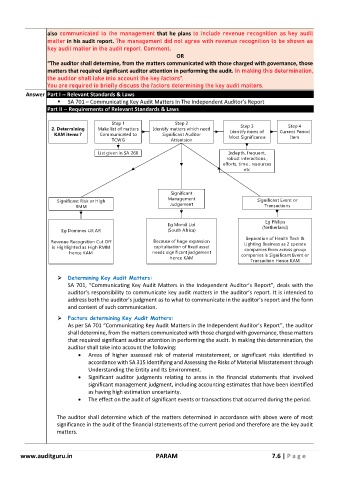

Step 1 Step 2 Step 3 Step 4

2. Determining Make list of matters Identify matters which need Identify items of Current Period

KAM items ? Communicated to Significant Auditor Most Significance Item

TCWG Attentsion

List given in SA 260 Indepth, frequent,

robust interactions ,

efforts, time , resources

etc

Significant

Significant Risk or High Management Significant Event or

RMM Judgement Transactions

Eg Philips

Eg Mondi Ltd (Netherland)

Eg Dominos UK AR (South Africa)

Separation of Health Tech &

Revenue Recognition Cut Off Because of huge expansion Lighting Business as 2 sperate

is Highlighted as High RMM capitalisation of fixed asset companies from across group

hence KAM needs significant judgement companies is Significant Event or

hence KAM

Transaction Hence KAM

➢ Determining Key Audit Matters:

SA 701, “Communicating Key Audit Matters in the Independent Auditor’s Report”, deals with the

auditor’s responsibility to communicate key audit matters in the auditor’s report. It is intended to

address both the auditor’s judgment as to what to communicate in the auditor’s report and the form

and content of such communication.

➢ Factors determining Key Audit Matters:

As per SA 701 “Communicating Key Audit Matters in the Independent Auditor’s Report”, the auditor

shall determine, from the matters communicated with those charged with governance, those matters

that required significant auditor attention in performing the audit. In making this determination, the

auditor shall take into account the following:

• Areas of higher assessed risk of material misstatement, or significant risks identified in

accordance with SA 315 Identifying and Assessing the Risks of Material Misstatement through

Understanding the Entity and Its Environment.

• Significant auditor judgments relating to areas in the financial statements that involved

significant management judgment, including accounting estimates that have been identified

as having high estimation uncertainty.

• The effect on the audit of significant events or transactions that occurred during the period.

The auditor shall determine which of the matters determined in accordance with above were of most

significance in the audit of the financial statements of the current period and therefore are the key audit

matters.

www.auditguru.in PARAM 7.6 | P a g e