Page 306 - CA Final PARAM Digital Book.

P. 306

but less than Rs 500 crore and holding, subsidiary, joint venture or associate

companies of such NBFCs.

o The net worth shall be calculated in accordance with the standalone financial

statements of the NBFCs as on 31st March 2016 or the first audited financial

statements for accounting period which ends after that date.

o Format for preparation of financial statements by NBFCs under Ind- AS –

The Ministry of Corporate Affairs (MCA) vide notification dated October 11, 2018

introduced Division III under Schedule III of the Companies Act, 2013, wherein a

format for preparation of financial statements by NBFCs complying with Ind-AS has

been prescribed.

➢ Differences Between Division Ii (Ind- AS- Other Than NBFCS) And Division Iii (Ind- AS-

NBFCS) of Schedule III

The presentation requirements under Division III for NBFCs are similar to Division II (Non NBFC) to a

large extent except for the following:

• Classification & Order in Balance Sheet

NBFCs have been allowed to present the items of the balance sheet in order of their liquidity

which is not allowed to companies required to follow Division II. Additionally, NBFCs are

required to classify items of the balance sheet into financial and non-financial whereas other

companies are required to classify the items into current and non-current.

• Material Items Disclosure

An NBFC is required to separately disclose by way of a note any item of ‘other income’ or

‘other expenditure’ which exceeds 1 per cent of the total income. Division II, on the other

hand, requires disclosure for any item of income or expenditure which exceeds 1 per cent of

the revenue from operations or Rs10 lakhs, whichever is higher.

• Separate Disclosures

o NBFCs are required to separately disclose under ‘receivables’, the debts due from

any Limited Liability Partnership (LLP) in which its director is a partner or member.

o Separate disclosure of trade receivable which have significant increase in credit

risk & credit impaired.

o The conditions or restrictions for distribution attached to statutory reserves have

to be separately disclose in the notes as stipulated by the relevant statute.

• Common Point

NBFCs are also required to disclose items comprising ‘revenue from operations’ and ‘other

comprehensive income’ on the face of the Statement of profit and loss instead of as part of

the notes

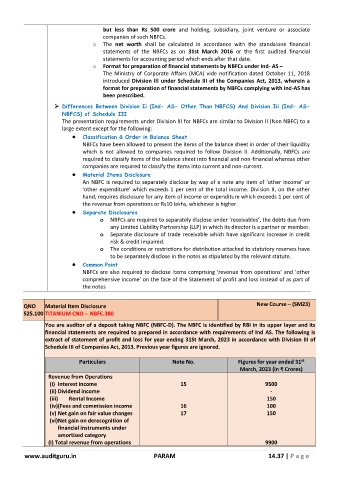

QNO Material Item Disclosure New Course – (SM23)

525.100 TITANIUM CNO -- NBFC.380

You are auditor of a deposit taking NBFC (NBFC-D). The NBFC is identified by RBI in its upper layer and its

financial statements are required to prepared in accordance with requirements of Ind AS. The following is

extract of statement of profit and loss for year ending 31St March, 2023 in accordance with Division III of

Schedule III of Companies Act, 2013. Previous year figures are ignored.

st

Particulars Note No. Figures for year ended 31

March, 2023 (in ₹ Crores)

Revenue from Operations

(i) Interest income 15 9500

(ii) Dividend income -

(iii) Rental Income 150

(iv) (Fees and commission income 16 100

(v) Net gain on fair value changes 17 150

(vi) Net gain on derecognition of

financial instruments under

amortised category

(I) Total revenue from operations 9900

www.auditguru.in PARAM 14.37 | P a g e