Page 34 - Chap24Computation of GST

P. 34

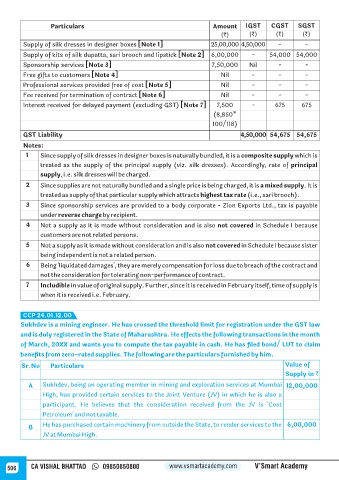

Particulars Amount IGST CGST SGST

(`) (`) (`) (`)

Supply of silk dresses in designer boxes [Note 1] 25,00,000 4,50,000 - -

Supply of kits of silk dupatta, sari brooch and lipstick [Note 2] 6,00,000 - 54,000 54,000

Sponsorship services [Note 3] 7,50,000 Nil - -

Free gifts to customers [Note 4] Nil - - -

Professional services provided free of cost [Note 5] Nil - - -

Fee received for termination of contract [Note 6] Nil - - -

Interest received for delayed payment (excluding GST) [Note 7] 7,500 - 675 675

(8,850*

100/118)

GST Liability 4,50,000 54,675 54,675

Notes:

1 Since supply of silk dresses in designer boxes is naturally bundled, it is a composite supply which is

treated as the supply of the principal supply (viz. silk dresses). Accordingly, rate of principal

supply, i.e. silk dresses will be charged.

2 Since supplies are not naturally bundled and a single price is being charged, it is a mixed supply. It is

treated as supply of that particular supply which attracts highest tax rate (i.e., sari brooch).

3 Since sponsorship services are provided to a body corporate - Zion Exports Ltd., tax is payable

under reverse charge by recipient.

4 Not a supply as it is made without consideration and is also not covered in Schedule I because

customers are not related persons.

5 Not a supply as it is made without consideration and is also not covered in Schedule I because sister

being independent is not a related person.

6 Being 'liquidated damages', they are merely compensation for loss due to breach of the contract and

not the consideration for tolerating non-performance of contract.

7 Includible in value of original supply. Further, since it is received in February itself, time of supply is

when it is received i.e. February.

CCP 24.01.12.00

Sukhdev is a mining engineer. He has crossed the threshold limit for registration under the GST law

and is duly registered in the State of Maharashtra. He effects the following transactions in the month

of March, 20XX and wants you to compute the tax payable in cash. He has filed bond/ LUT to claim

benefits from zero-rated supplies. The following are the particulars furnished by him.

Sr.No Particulars Value of

Supply in `

A Sukhdev, being an operating member in mining and exploration services at Mumbai 12,00,000

High, has provided certain services to the Joint Venture (JV) in which he is also a

participant. He believes that the consideration received from the JV is 'Cost

Petroleum' and not taxable.

He has purchased certain machinery from outside the State, to render services to the 6,00,000

B

JV at Mumbai High.

506 CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy