Page 35 - Chap24Computation of GST

P. 35

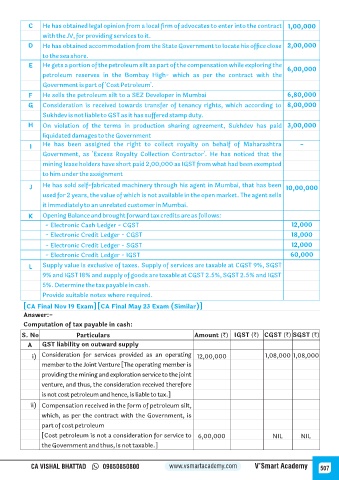

C He has obtained legal opinion from a local firm of advocates to enter into the contract 1,00,000

with the JV, for providing services to it.

D He has obtained accommodation from the State Government to locate his office close 2,00,000

to the sea shore.

E He gets a portion of the petroleum silt as part of the compensation while exploring the

6,00,000

petroleum reserves in the Bombay High- which as per the contract with the

Government is part of 'Cost Petroleum'.

F He sells the petroleum silt to a SEZ Developer in Mumbai 6,80,000

G Consideration is received towards transfer of tenancy rights, which according to 8,00,000

Sukhdev is not liable to GST as it has suffered stamp duty.

H On violation of the terms in production sharing agreement, Sukhdev has paid 3,00,000

liquidated damages to the Government

He has been assigned the right to collect royalty on behalf of Maharashtra -

I

Government, as 'Excess Royalty Collection Contractor'. He has noticed that the

mining lease holders have short paid 2,00,000 as IGST from what had been exempted

to him under the assignment

J He has sold self-fabricated machinery through his agent in Mumbai, that has been 10,00,000

used for 2 years, the value of which is not available in the open market. The agent sells

it immediately to an unrelated customer in Mumbai.

K Opening Balance and brought forward tax credits are as follows:

- Electronic Cash Ledger - CGST 12,000

- Electronic Credit Ledger - CGST 18,000

- Electronic Credit Ledger - SGST 12,000

- Electronic Credit Ledger - IGST 60,000

L Supply value is exclusive of taxes. Supply of services are taxable at CGST 9%, SGST

9% and IGST 18% and supply of goods are taxable at CGST 2.5%, SGST 2.5% and IGST

5%. Determine the tax payable in cash.

Provide suitable notes where required.

[CA Final Nov 19 Exam] [CA Final May 23 Exam (Similar)]

Answer:-

Computation of tax payable in cash:

S. No Particulars Amount (`) IGST (`) CGST (`) SGST (`)

A GST liability on outward supply

i) Consideration for services provided as an operating 12,00,000 1,08,000 1,08,000

member to the Joint Venture [The operating member is

providing the mining and exploration service to the joint

venture, and thus, the consideration received therefore

is not cost petroleum and hence, is liable to tax.]

ii) Compensation received in the form of petroleum silt,

which, as per the contract with the Government, is

part of cost petroleum

[Cost petroleum is not a consideration for service to 6,00,000 NIL NIL

the Government and thus, is not taxable.]

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 507