Page 28 - Chap7 ITC

P. 28

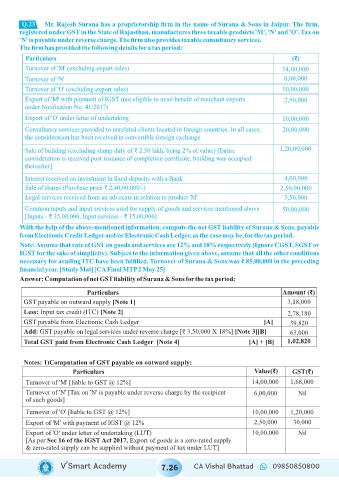

Q.23

3 Mr. Rajesh Surana has a proprietorship firm in the name of Surana & Sons in Jaipur. The firm,

registered under GST in the State of Rajasthan, manufactures three taxable products 'M', 'N' and 'O'. Tax on

'N' is payable under reverse charge. The firm also provides taxable consultancy services.

The firm has provided the following details for a tax period:

Particulars (₹)

Turnover of 'M' (excluding export sales) 14,00,000

Turnover of 'N' 6,00,000

Turnover of 'O' (excluding export sales) 10,00,000

Export of 'M' with payment of IGST (not eligible to avail benefit of merchant exports 2,50,000

under Notification No. 41/2017)

Export of 'O' under letter of undertaking 10,00,000

Consultancy services provided to unrelated clients located in foreign countries. In all cases, 20,00,000

the consideration has been received in convertible foreign exchange

Sale of building (excluding stamp duty of ₹ 2.50 lakh, being 2% of value) [Entire 1,20,00,000

consideration is received post issuance of completion certificate, building was occupied

thereafter]

Interest received on investment in fixed deposits with a Bank 4,00,000

Sale of shares (Purchase price ₹ 2,40,00,000/-) 2,50,00,000

Legal services received from an advocate in relation to product 'M' 3,50,000

Common inputs and input services used for supply of goods and services mentioned above 50,00,000

[Inputs - ₹ 35,00,000, Input services - ₹ 15,00,000]

With the help of the above-mentioned information, compute the net GST liability of Surana & Sons, payable

from Electronic Credit Ledger and/or Electronic Cash Ledger, as the case may be, for the tax period.

Note: Assume that rate of GST on goods and services are 12% and 18% respectively (Ignore CGST, SGST or

IGST for the sake of simplicity). Subject to the information given above, assume that all the other conditions

necessary for availing ITC have been fulfilled. Turnover of Surana & Sons was ₹ 85,00,000 in the preceding

financial year. [Study Mat] [CA Final MTP 2 May 25]

Answer: Computation of net GST liability of Surana & Sons for the tax period:

Particulars Amount (₹)

GST payable on outward supply [Note 1] 3,18,000

Less: Input tax credit (ITC) [Note 2] 2,78,180

GST payable from Electronic Cash Ledger [A] 39,820

Add: GST payable on legal services under reverse charge [₹ 3,50,000 X 18%] [Note 3][B] 63,000

Total GST paid from Electronic Cash Ledger [Note 4] [A] + [B] 1,02,820

Notes: 1) Computation of GST payable on outward supply:

Particulars Value(₹) GST(₹)

Turnover of 'M' [liable to GST @ 12%] 14,00,000 1,68,000

Turnover of 'N' [Tax on 'N' is payable under reverse charge by the recipient 6,00,000 Nil

of such goods]

Turnover of 'O' [liable to GST @ 12%] 10,00,000 1,20,000

Export of 'M' with payment of IGST @ 12% 2,50,000 30,000

Export of 'O' under letter of undertaking (LUT) 10,00,000 Nil

[As per Sec 16 of the IGST Act 2017, Export of goods is a zero-rated supply

& zero-rated supply can be supplied without payment of tax under LUT]

V’Smart Academy 7.26 CA Vishal Bhattad 09850850800