Page 42 - Chap7 ITC

P. 42

2. IGST credit of ₹ 1,50,000, CGST credit of ₹ 15,000 and SGST credit of ₹ 15,000 specifically attributable

to Mumbai Branch, Maharashtra will be distributed as IGST credit of ₹ 1,50,000, CGST credit of ₹

15,000 and SGST credit of ₹ 15,000 respectively, only to Mumbai Branch, Maharashtra [Since recipient

is located in the same State in which ISD is located].

3. CGST credit of ₹ 60,000, SGST credit of ₹ 60,000 and IGST credit of ₹ 1,20,000 have to be distributed

among the three branches and Mumbai Branch, Maharashtra in proportion of their turnover of the last

quarter.

Ü Ganganagar Branch, Rajasthan will get: ₹ 48,000 [₹ 2,40,000 x (₹ 10,00,000/ ₹ 50,00,000)] as IGST

credit.

Ü Madhugiri Branch, Karnataka will get: ₹ 24,000 [₹ 2,40,000 x (₹ 5,00,000/ ₹ 50,00,000)] as IGST

credit.

Ü The credit attributable to a recipient is distributed even if such recipient is making exempt supplies.

Ü Kosala Branch, UP will get: ₹ 72,000 [₹ 2,40,000 x (₹ 15,00,000/ ₹ 50,00,000)] as IGST credit.

Ü Mumbai Branch, Maharashtra will get:

₹ 24,000 [₹ 60,000 x (₹ 20,00,000/ ₹ 50,00,000)] as CGST credit,

₹ 24,000 [₹ 60,000 x (₹ 20,00,000/ ₹ 50,00,000)] as SGST credit and

₹ 48,000 [₹ 1,20,000 x (₹ 20,00,000/ ₹ 50,00,000)] as IGST credit.

4. ITC of ₹ 10,000 of March (last year) cannot be distributed in March this year as ITC available for

distribution in a month is to be distributed in the same month.

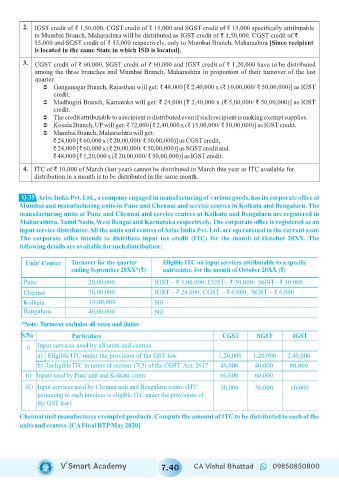

Q.35

Arise India Pvt. Ltd., a company engaged in manufacturing of various goods, has its corporate office at

Mumbai and manufacturing units in Pune and Chennai and service centres in Kolkata and Bengaluru. The

manufacturing units at Pune and Chennai and service centres at Kolkata and Bengaluru are registered in

Maharashtra, Tamil Nadu, West Bengal and Karnataka respectively. The corporate office is registered as an

input service distributor. All the units and centres of Arise India Pvt. Ltd. are operational in the current year.

The corporate office intends to distribute input tax credit (ITC) for the month of October 20XX. The

following details are available for such distribution :

Unit/ Center Turnover for the quarter Eligible ITC on input services attributable to a specific

ending September 20XX*(₹) unit/center, for the month of October 20XX (₹)

Pune 20,00,000 IGST – ₹ 3,00,000; CGST– ₹ 30,000; SGST– ₹ 30,000

Chennai 30,00,000 IGST – ₹ 24,000; CGST – ₹ 6,000; SGST – ₹ 6,000

Kolkata 10,00,000 Nil

Bengaluru 40,00,000 Nil

*Note: Turnover excludes all taxes and duties

S.No Particulars CGST SGST IGST

i) Input services used by all units and centres

a) Eligible ITC under the provision of the GST law 1,20,000 1,20,000 2,40,000

b) Ineligible ITC in terms of section 17(5) of the CGST Act, 2017 40,000 40,000 80,000

ii) Inputs used by Pune unit and Kolkata centre 60,000 60,000

iii) Input services used by Chennai unit and Bengaluru centre (ITC 30,000 30,000 10,000

pertaining to such invoices is eligible ITC under the provisions of

the GST law)

Chennai unit manufactures exempted products. Compute the amount of ITC to be distributed to each of the

units and centres. [CA Final RTP May 2020]

V’Smart Academy 7.40 CA Vishal Bhattad 09850850800