Page 123 - CA Inter Audit PARAM

P. 123

CA Ravi Taori

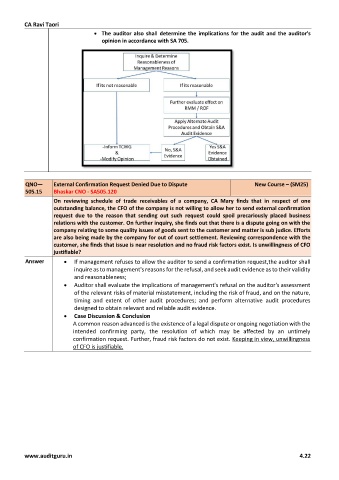

• The auditor also shall determine the implications for the audit and the auditor’s

opinion in accordance with SA 705.

QNO— External Confirmation Request Denied Due to Dispute New Course – (SM25)

505.15 Bhaskar CNO - SA505.120

On reviewing schedule of trade receivables of a company, CA Mary finds that in respect of one

outstanding balance, the CFO of the company is not willing to allow her to send external confirmation

request due to the reason that sending out such request could spoil precariously placed business

relations with the customer. On further inquiry, she finds out that there is a dispute going on with the

company relating to some quality issues of goods sent to the customer and matter is sub judice. Efforts

are also being made by the company for out of court settlement. Reviewing correspondence with the

customer, she finds that issue is near resolution and no fraud risk factors exist. Is unwillingness of CFO

justifiable?

Answer • If management refuses to allow the auditor to send a confirmation request,the auditor shall

inquire as to management's reasons for the refusal, and seek audit evidence as to their validity

and reasonableness;

• Auditor shall evaluate the implications of management's refusal on the auditor's assessment

of the relevant risks of material misstatement, including the risk of fraud, and on the nature,

timing and extent of other audit procedures; and perform alternative audit procedures

designed to obtain relevant and reliable audit evidence.

• Case Discussion & Conclusion

A common reason advanced is the existence of a legal dispute or ongoing negotiation with the

intended confirming party, the resolution of which may be affected by an untimely

confirmation request. Further, fraud risk factors do not exist. Keeping in view, unwillingness

of CFO is justifiable.

www.auditguru.in 4.22