Page 5 - Chapter 10 Registration

P. 5

Answer:- CCP 10.02.05.00

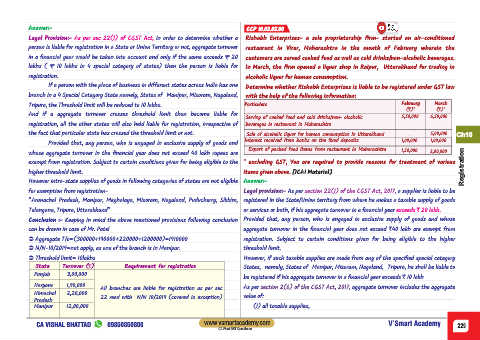

Legal Provision:- As per sec 22(1) of CGST Act, in order to determine whether a Rishabh Enterprises- a sole proprietorship firm- started an air-conditioned

person is liable for registration in a State or Union Territory or not, aggregate turnover restaurant in Virar, Maharashtra in the month of February wherein the

in a financial year would be taken into account and only if the same exceeds ₹ 20 customers are served cooked food as well as cold drinks/non-alcoholic beverages.

lakhs ( ₹ 10 lakhs in 4 special category of states) then the person is liable for In March, the firm opened a liquor shop in Raipur, Uttarakhand for trading in

registration. alcoholic liquor for human consumption.

If a person with the place of business in different states across India has one Determine whether Rishabh Enterprises is liable to be registered under GST law

branch in a 4 Special Category State namely, States of Manipur, Mizoram, Nagaland, with the help of the following information:

Tripura, the Threshold limit will be reduced to 10 lakhs. Particulars February March

(`)* (`)*

And if a aggregate turnover crosses threshold limit than become liable for

Serving of cooked food and cold drinks/non- alcoholic 5,50,000 6,50,000

registration, all the other states will also held liable for registration, irrespective of beverages in restaurant in Maharashtra

the fact that particular state has crossed the threshold limit or not. Sale of alcoholic liquor for human consumption in Uttarakhand - 5,00,000 Ch10

Interest received from banks on the fixed deposits 1,00,000 1,00,000

Provided that, any person, who is engaged in exclusive supply of goods and

Export of packed food items from restaurant in Maharashtra

whose aggregate turnover in the financial year does not exceed 40 lakh rupees are 1,50,000 2,00,000

exempt from registration. Subject to certain conditions given for being eligible to the * excluding GST, You are required to provide reasons for treatment of various

higher threshold limit. items given above. [ICAI Material] Registration

However intra-state supplies of goods in following categories of states are not eligible Answer:-

for exemption from registration- Legal provision:- As per section 22(1) of the CGST Act, 2017, a supplier is liable to be

“Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, Puducherry, Sikkim, registered in the State/Union territory from where he makes a taxable supply of goods

Telangana, Tripura, Uttarakhand” or services or both, if his aggregate turnover in a financial year exceeds ` 20 lakh.

Conclusion :- Keeping in mind the above mentioned provisions following conclusion Provided that, any person, who is engaged in exclusive supply of goods and whose

can be drawn in case of Mr. Patel aggregate turnover in the financial year does not exceed `40 lakh are exempt from

Ü Aggregate T/o=(300000+190000+220000+1200000)=1910000 registration. Subject to certain conditions given for being eligible to the higher

Ü N/N-10/2019=not apply, as one of the branch is in Manipur. threshold limit.

Ü Threshold limit= 10lakhs However, if such taxable supplies are made from any of the specified special category

State Turnover (`) Requirement for registration States, namely, States of Manipur, Mizoram, Nagaland, Tripura, he shall be liable to

Punjab 3,00,000

be registered if his aggregate turnover in a financial year exceeds ` 10 lakh

Haryana 1,90,000 As per section 2(6) of the CGST Act, 2017, aggregate turnover includes the aggregate

All branches are liable for registration as per sec

Himachal 2,20,000

22 read with N/N 10/2019 (covered in exception) value of:

Pradesh

Manipur 12,00,000 (I) all taxable supplies,

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 229

CA Final GST Questioner