Page 6 - Chapter 10 Registration

P. 6

(ii) all exempt supplies (which includes wholly exempt, Nil rated & Non-taxable being a non-taxable supply, is an exempt supply and is, therefore, includible while

supply ), computing the aggregate turnover.

(iii) exports of goods and/or services and 2. Services by way of extending deposits, loans or advances in so far as the

(iv) all inter-State supplies of persons having the same PAN. consideration is represented by way of interest or discount (other than interest

The above is computed on all India basis. Further, the aggregate turnover excludes involved in credit card services) is exempt vide Notification No. 12/2017 CT (R)

Central tax, State tax, Union territory tax, Integrated tax and cess. Moreover, the value dated 28.06.2017. Thus, interest received from banks on the fixed deposits is an

of inward supplies on which tax is payable under reverse charge is not taken into exempt supply and is, therefore, includible while computing the aggregate turnover.

account for calculation of 'aggregate turnover'. Conclusion:-In the given case, Since Rishabh Enterprises was not liable to be

In the given question, since Rishabh Enterprises is engaged in making taxable registered in the month of February since its aggregate turnover did not exceed ` 20

supplies from Maharashtra which is not a specified Special Category State, the lakh in that month. However, since its aggregate turnover exceeds ` 20 lakh in the

threshold limit for obtaining registration is ` 20 lakh. month of March, it should apply for registration within 30 days from the date on

Supply of alcoholic liquor are non-taxable supplies in terms of section 9(1) of CGST

CH 10 which it becomes liable to registration.

Act, 2017.

Further as per sec 23, he is not liable to be registered in Uttarakhand since he

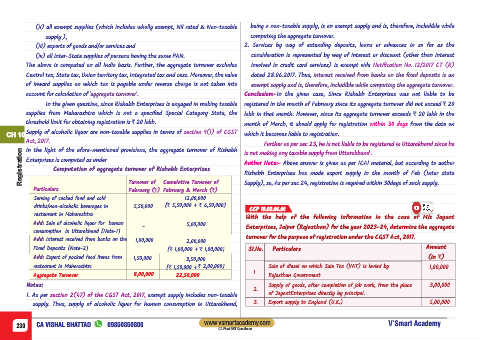

Registration Enterprises is computed as under Author Note:- Above answer is given as per ICAI material, but according to author

In the light of the afore-mentioned provisions, the aggregate turnover of Rishabh

is not making any taxable supply from Uttarakhand .

Computation of aggregate turnover of Rishabh Enterprises

Rishabh Enterprises has made export supply in the month of Feb (Inter state

Particulars Turnover of Cumulative Turnover of Supply), so, As per sec 24, registration is required within 30days of such supply.

February (`) February & March (`)

Serving of cooked food and cold 12,00,000

drinks/non-alcoholic beverages in 5,50,000 [` 5,50,000 + ` 6,50,000]

CCP 10.02.06.00

restaurant in Maharashtra

With the help of the following information in the case of M/s Jayant

Add: Sale of alcoholic liquor for human 5,00,000

- Enterprises, Jaipur (Rajasthan) for the year 2023-24, determine the aggregate

consumption in Uttarakhand [Note-1]

turnover for the purpose of registration under the CGST Act, 2017.

Add: Interest received from banks on the 1,00,000 2,00,000

Fixed Deposits [Note-2] [` 1,00,000 + ` 1,00,000] SI.No. Particulars Amount

Add: Export of packed food items from 1,50,000 3,50,000 (in `)

restaurant in Maharashtra [` 1,50,000 + ` 2,00,000] Sale of diesel on which Sale Tax (VAT) is levied by 1,00,000

1

Aggregate Turnover 8,00,000 22,50,000 Rajasthan Government

Notes: Supply of goods, after completion of job work, from the place 3,00,000

2.

1. As per section 2(47) of the CGST Act, 2017, exempt supply includes non-taxable of JayantEnterprises directly by principal.

supply. Thus, supply of alcoholic liquor for human consumption in Uttarakhand, 3. Export supply to England (U.K.) 5,00,000

www.vsmartacademy.com

230 CA VISHAL BHATTAD 09850850800 V’Smart Academy

CA Final GST Questioner