Page 8 - Chapter 10 Registration

P. 8

CCP 10.02.08.00 Also, as per section 2(6) of the CGST Act, 2017, aggregate turnover includes the

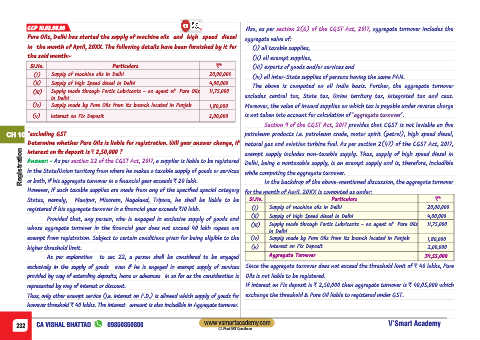

Pure Oils, Delhi has started the supply of machine oils and high speed diesel aggregate value of:

in the month of April, 20XX. The following details have been furnished by it for (i) all taxable supplies,

the said month:- (ii) all exempt supplies,

SI.No. Particulars `* (iii) exports of goods and/or services and

(I) Supply of machine oils in Delhi 20,00,000 (iv) all inter-State supplies of persons having the same PAN.

(ii) Supply of high Speed diesel in Delhi 4,00,000

The above is computed on all India basis. Further, the aggregate turnover

(iii) Supply made through Fortis Lubricants - an agent of Pure Oils 11,75,000

in Delhi excludes central tax, State tax, Union territory tax, integrated tax and cess.

(iv) Supply made by Pure Oils from its branch located in Punjab 1,80,000 Moreover, the value of inward supplies on which tax is payable under reverse charge

(v) Interest on Fix Deposit 2,00,000 is not taken into account for calculation of ‘aggregate turnover’.

Section 9 of the CGST Act, 2017 provides that CGST is not leviable on five

CH 10 *excluding GST petroleum products i.e. petroleum crude, motor spirit (petrol), high speed diesel,

Determine whether Pure Oils is liable for registration. Will your answer change, if natural gas and aviation turbine fuel. As per section 2(47) of the CGST Act, 2017,

Registration Answer: - As per section 22 of the CGST Act, 2017 , a supplier is liable to be registered Delhi, being a nontaxable supply, is an exempt supply and is, therefore, includible

interest on fix deposit is ` 2,50,000 ?

exempt supply includes non-taxable supply. Thus, supply of high speed diesel in

in the State/Union territory from where he makes a taxable supply of goods or services

while computing the aggregate turnover.

or both, if his aggregate turnover in a financial year exceeds ` 20 lakh.

In the backdrop of the above-mentioned discussion, the aggregate turnover

However, if such taxable supplies are made from any of the specified special category for the month of April, 20XX is computed as under:

States, namely, Manipur, Mizoram, Nagaland, Tripura, he shall be liable to be SI.No. Particulars `*

registered if his aggregate turnover in a financial year exceeds `10 lakh. (I) Supply of machine oils in Delhi 20,00,000

Provided that, any person, who is engaged in exclusive supply of goods and (ii) Supply of high Speed diesel in Delhi 4,00,000

(iii) Supply made through Fortis Lubricants - an agent of Pure Oils 11,75,000

whose aggregate turnover in the financial year does not exceed 40 lakh rupees are

in Delhi

exempt from registration. Subject to certain conditions given for being eligible to the (iv) Supply made by Pure Oils from its branch located in Punjab 1,80,000

higher threshold limit. (v) Interest on Fix Deposit 2,00,000

As per explanation to sec 22, a person shall be considered to be engaged Aggregate Turnover 39,55,000

exclusively in the supply of goods even if he is engaged in exempt supply of services Since the aggregate turnover does not exceed the threshold limit of ` 40 lakhs, Pure

provided by way of extending deposits, loans or advances in so far as the consideration is Oils is not liable to be registered.

represented by way of interest or discount. If interest on Fix deposit is ` 2,50,000 then aggregate turnover is ` 40,05,000 which

Thus, only other exempt service (i.e. interest on F.D.) is allowed which supply of goods for exchange the threshold & Pure Oil liable to registered under GST.

however threshold ` 40 lakhs. The interest amount is also includible in Aggregate turnover.

www.vsmartacademy.com

232 CA VISHAL BHATTAD 09850850800 V’Smart Academy

CA Final GST Questioner