Page 9 - Chapter 10 Registration

P. 9

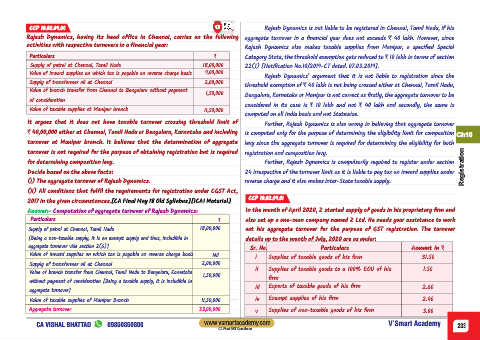

CCP 10.02.09.00 Rajesh Dynamics is not liable to be registered in Chennai, Tamil Nadu, if his

Rajesh Dynamics, having its head office in Chennai, carries on the following aggregate turnover in a financial year does not exceeds ` 40 lakh. However, since

activities with respective turnovers in a financial year: Rajesh Dynamics also makes taxable supplies from Manipur, a specified Special

Particulars ` Category State, the threshold exemption gets reduced to ` 10 lakh in terms of section

Supply of petrol at Chennai, Tamil Nadu 18,00,000 22(1) [Notification No.10/2019-CT dated. 07.03.2019].

Value of inward supplies on which tax is payable on reverse charge basis 9,00,000

Rajesh Dynamics’ argument that it is not liable to registration since the

Supply of transformer oil at Chennai 2,00,000

threshold exemption of ` 40 lakh is not being crossed either at Chennai, Tamil Nadu,

Value of branch transfer from Chennai to Bengaluru without payment

1,50,000 Bengaluru, Karnataka or Manipur is not correct as firstly, the aggregate turnover to be

of consideration

considered in its case is ` 10 lakh and not ` 40 lakh and secondly, the same is

Value of taxable supplies at Manipur branch 11,50,000

computed on all India basis and not Statewise.

It argues that it does not have taxable turnover crossing threshold limit of Further, Rajesh Dynamics is also wrong in believing that aggregate turnover

` 40,00,000 either at Chennai, Tamil Nadu or Bengaluru, Karnataka and including is computed only for the purpose of determining the eligibility limit for composition

Ch10

turnover at Manipur branch. It believes that the determination of aggregate levy since the aggregate turnover is required for determining the eligibility for both

turnover is not required for the purpose of obtaining registration but is required registration and composition levy.

for determining composition levy. Further, Rajesh Dynamics is compulsorily required to register under section Registration

Decide based on the above facts: 24 irrespective of the turnover limit as it is liable to pay tax on inward supplies under

(i) The aggregate turnover of Rajesh Dynamics. reverse charge and it also makes inter-State taxable supply.

(ii) All conditions that fulfil the requirements for registration under CGST Act,

CCP 10.02.09.01

2017 in the given circumstances.[CA Final May 18 Old Syllabus][ICAI Material]

Answer:- Computation of aggregate turnover of Rajesh Dynamics: In the month of April 2020, Z started supply of goods in his proprietary firm and

Particulars ` also set up a one-man company named Z Ltd. He needs your assistance to work

Supply of petrol at Chennai, Tamil Nadu 18,00,000 out his aggregate turnover for the purpose of GST registration. The turnover

[Being a non-taxable supply, it is an exempt supply and thus, includible in details up to the month of July, 2020 are as under:

aggregate turnover vide section 2(6)] Sr. No. Particulars Amount in `

Value of inward supplies on which tax is payable on reverse charge basis Nil Supplies of taxable goods of his firm

i 31.50

Supply of transformer oil at Chennai 2,00,000

ii Supplies of taxable goods to a 100% EOU of his 1.50

Value of branch transfer from Chennai, Tamil Nadu to Bengaluru, Karnataka

1,50,000

firm

without payment of consideration [Being a taxable supply, it is includible in

iii Exports of taxable goods of his firm 2.60

aggregate turnover]

Value of taxable supplies of Manipur Branch 11,50,000 iv Exempt supplies of his firm 2.40

Aggregate turnover 33,00,000 v Supplies of non-taxable goods of his firm 3.00

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 233

CA Final GST Questioner