Page 10 - Chapter 10 Registration

P. 10

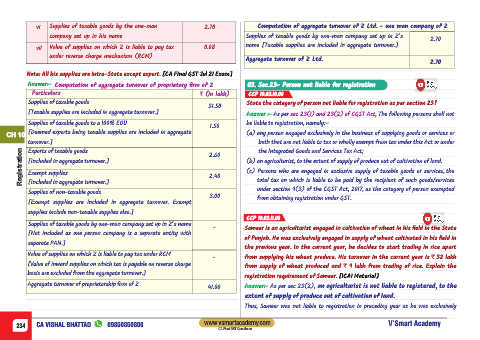

vi Supplies of taxable goods by the one-man 2.70 Computation of aggregate turnover of Z Ltd. - one man company of Z

company set up in his name Supplies of taxable goods by one-man company set up in Z’s

2.70

vii Value of supplies on which Z is liable to pay tax 0.08 name [Taxable supplies are included in aggregate turnover.]

under reverse charge mechanism (RCM)

Aggregate turnover of Z Ltd.

2.70

Note: All his supplies are intra-State except export. [CA Final GST Jul 21 Exam]

Answer:- Computation of aggregate turnover of proprietary firm of Z 03. Sec.23- Person not liable for registration

Particulars ` (in lakh) CCP 10.03.10.00

Supplies of taxable goods State the category of person not liable for registration as per section 23?

31.50

[Taxable supplies are included in aggregate turnover.] Answer :- As per sec 23(1) and 23(2) of CGST Act, The following persons shall not

Supplies of taxable goods to a 100% EOU be liable to registration, namely:–

1.50

CH 10 [Deemed exports being taxable supplies are included in aggregate (a) any person engaged exclusively in the business of supplying goods or services or

turnover.] both that are not liable to tax or wholly exempt from tax under this Act or under

Registration [Included in aggregate turnover.] 2.60 (b) an agriculturist, to the extent of supply of produce out of cultivation of land.

the Integrated Goods and Services Tax Act;

Exports of taxable goods

(c) Persons who are engaged in exclusive supply of taxable goods or services, the

Exempt supplies

2.40

total tax on which is liable to be paid by the recipient of such goods/services

[Included in aggregate turnover.]

under section 9(3) of the CGST Act, 2017, as the category of person exempted

Supplies of non-taxable goods

3.00 from obtaining registration under GST.

[Exempt supplies are included in aggregate turnover. Exempt

supplies include non-taxable supplies also.]

CCP 10.03.11.00

Supplies of taxable goods by one-man company set up in Z’s name

- Sameer is an agriculturist engaged in cultivation of wheat in his field in the State

[Not included as one person company is a separate entity with

of Punjab. He was exclusively engaged in supply of wheat cultivated in his field in

separate PAN.]

the previous year. In the current year, he decides to start trading in rice apart

Value of supplies on which Z is liable to pay tax under RCM

- from supplying his wheat produce. His turnover in the current year is ` 32 lakh

[Value of inward supplies on which tax is payable on reverse charge

from supply of wheat produced and ` 9 lakh from trading of rice. Explain the

basis are excluded from the aggregate turnover.]

registration requirement of Sameer. [ICAI Material]

Aggregate turnover of proprietorship firm of Z Answer:- As per sec 23(2), an agriculturist is not liable to registered, to the

41.00

extent of supply of produce out of cultivation of land.

Thus, Sameer was not liable to registration in preceding year as he was exclusively

www.vsmartacademy.com

234 CA VISHAL BHATTAD 09850850800 V’Smart Academy

CA Final GST Questioner