Page 25 - Chapter 2.cdr

P. 25

2. The transportation of the generators from Jaskaran's warehouse to the Notes :-

customer's premises is arranged by Jaskaran through a Goods Transport 1. As per section 2(74) of the CGST Act, 2017, mixed supply means two or more

Agency (GTA) who pays tax @ 12%. individual supplies of goods or services, or any combination thereof, made in CH 2

3. Assume the rates of GST to be as under:( CA Final RTP Nov 2018) conjunction with each other by a taxable person for a single price where such

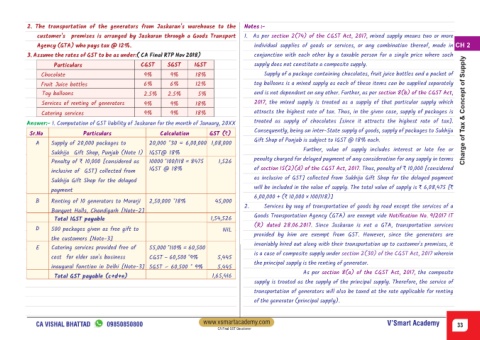

Particulars CGST SGST IGST supply does not constitute a composite supply.

Chocolate 9% 9% 18% Supply of a package containing chocolates, fruit juice bottles and a packet of

Fruit Juice bottles 6% 6% 12% toy balloons is a mixed supply as each of these items can be supplied separately

Toy balloons 2.5% 2.5% 5% and is not dependent on any other. Further, as per section 8(b) of the CGST Act,

Services of renting of generators 9% 9% 18% 2017, the mixed supply is treated as a supply of that particular supply which

Catering services 9% 9% 18% attracts the highest rate of tax. Thus, in the given case, supply of packages is Charge of Tax & Concept of Supply

treated as supply of chocolates [since it attracts the highest rate of tax].

Answer:- 1. Computation of GST liability of Jaskaran for the month of January, 20XX

Consequently, being an inter-State supply of goods, supply of packages to Sukhija

Sr.No Particulars Calculation GST (`)

Gift Shop of Punjab is subject to IGST @ 18% each.

A Supply of 20,000 packages to 20,000 *30 = 6,00,000 1,08,000

Further, value of supply includes interest or late fee or

Sukhija Gift Shop, Punjab (Note 1) IGST@ 18%

penalty charged for delayed payment of any consideration for any supply in terms

Penalty of ` 10,000 [considered as 10000 *100/118 = 8475 1,526

IGST @ 18% of section 15(2)(d) of the CGST Act, 2017. Thus, penalty of ` 10,000 [considered

inclusive of GST] collected from

as inclusive of GST] collected from Sukhija Gift Shop for the delayed payment

Sukhija Gift Shop for the delayed

will be included in the value of supply. The total value of supply is ` 6,08,475 [`

payment

6,00,000 + (` 10,000 × 100/118)]

B Renting of 10 generators to Morarji 2,50,000 *18% 45,000

2. Services by way of transportation of goods by road except the services of a

Banquet Halls, Chandigarh [Note-2]

Goods Transportation Agency (GTA) are exempt vide Notification No. 9/2017 IT

Total IGST payable 1,54,526

(R) dated 28.06.2017. Since Jaskaran is not a GTA, transportation services

D 500 packages given as free gift to NIL

provided by him are exempt from GST. However, since the generators are

the customers [Note-3]

invariably hired out along with their transportation up to customer's premises, it

E Catering services provided free of 55,000 *110% = 60,500

is a case of composite supply under section 2(30) of the CGST Act, 2017 wherein

cost for elder son's business CGST – 60,500 *9% 5,445

the principal supply is the renting of generator.

inaugural function in Delhi [Note-3] SGST – 60,500 * 9% 5,445

As per section 8(a) of the CGST Act, 2017, the composite

Total GST payable (c+d+e) 1,65,416

supply is treated as the supply of the principal supply. Therefore, the service of

transportation of generators will also be taxed at the rate applicable for renting

of the generator (principal supply).

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 33

CA Final GST Questioner