Page 18 - 10. COMPILER QB - INDAS 36

P. 18

(iv) If the value in use was zero and the company was required to incur a cost of Rs8 lakh to dispose of the

plant, what would be your response to questions (i) and (ii) above?

SOLUTION

As per the requirement of the question, the following solution has been drawn on the basis

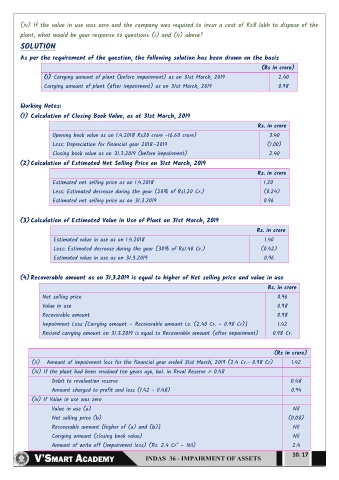

(Rs in crore)

(i) Carrying amount of plant (before impairment) as on 31st March, 2019 2.40

Carrying amount of plant (after impairment) as on 31st March, 2019 0.98

Working Notes:

(1) Calculation of Closing Book Value, as at 31st March, 2019

Rs. in crore

Opening book value as on 1.4.2018 Rs20 crore -16.60 crore) 3.40

Less: Depreciation for financial year 2018–2019 (1.00)

Closing book value as on 31.3.2019 (before impairment) 2.40

(2) Calculation of Estimated Net Selling Price on 31st March, 2019

Rs. in crore

Estimated net selling price as on 1.4.2018 1.20

Less: Estimated decrease during the year (20% of Rs1.20 Cr.) (0.24)

Estimated net selling price as on 31.3.2019 0.96

(3) Calculation of Estimated Value in Use of Plant on 31st March, 2019

Rs. in crore

Estimated value in use as on 1.4.2018 1.40

Less: Estimated decrease during the year (30% of Rs1.40 Cr.) (0.42)

Estimated value in use as on 31.3.2019 0.96

(4) Recoverable amount as on 31.3.2019 is equal to higher of Net selling price and value in use

Rs. in crore

Net selling price 0.96

Value in use 0.98

Recoverable amount 0.98

Impairment Loss [Carrying amount – Recoverable amount i.e. (2.40 Cr. – 0.98 Cr)] 1.42

Revised carrying amount on 31.3.2019 is equal to Recoverable amount (after impairment) 0.98 Cr.

(Rs in crore)

(ii) Amount of impairment loss for the financial year ended 31st March, 2019 (2.4 Cr.- 0.98 Cr) 1.42

(iii) If the plant had been revalued ten years ago, bal. in Reval Reserve = 0.48

Debit to revaluation reserve 0.48

Amount charged to profit and loss (1.42 - 0.48) 0.94

(iv) If Value in use was zero

Value in use (a) Nil

Net selling price (b) (0.08)

Recoverable amount [higher of (a) and (b)] Nil

Carrying amount (closing book value) Nil

Amount of write off (impairment loss) (Rs. 2.4 Cr* – Nil) 2.4

10. 17