Page 17 - 10. COMPILER QB - INDAS 36

P. 17

note - don’t do (d+f). ‘d’ is just for allocation purposes. Carrying amount will be the same as before

allocating the amount of AU

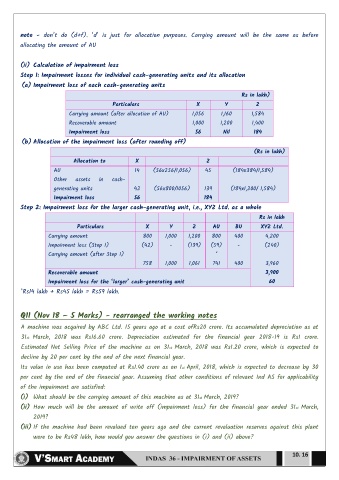

(ii) Calculation of impairment loss

Step 1: Impairment losses for individual cash-generating units and its allocation

(a) Impairment loss of each cash-generating units

Rs in lakh)

Particulars X Y Z

Carrying amount (after allocation of AU) 1,056 1,160 1,584

Recoverable amount 1,000 1,200 1,400

Impairment loss 56 Nil 184

(b) Allocation of the impairment loss (after rounding off)

(Rs in lakh)

Allocation to X Z

AU 14 (56x256/1,056) 45 (184x384/1,584)

Other assets in cash-

generating units 42 (56x800/1056) 139 (184x1,200/ 1,584)

Impairment loss 56 184

Step 2: Impairment loss for the larger cash-generating unit, i.e., XYZ Ltd. as a whole

Rs in lakh

Particulars X Y Z AU BU XYZ Ltd.

Carrying amount 800 1,000 1,200 800 400 4,200

Impairment loss (Step I) (42) - (139) (59) - (240)

Carrying amount (after Step I) *

758 1,000 1,061 741 400 3,960

Recoverable amount 3,900

Impairment loss for the ‘larger’ cash-generating unit 60

*Rs14 lakh + Rs45 lakh = Rs59 lakh.

Q11 (Nov 18 – 5 Marks) - rearranged the working notes

A machine was acquired by ABC Ltd. 15 years ago at a cost ofRs20 crore. Its accumulated depreciation as at

31st March, 2018 was Rs16.60 crore. Depreciation estimated for the financial year 2018-19 is Rs1 crore.

Estimated Net Selling Price of the machine as on 31st March, 2018 was Rs1.20 crore, which is expected to

decline by 20 per cent by the end of the next financial year.

Its value in use has been computed at Rs1.40 crore as on 1st April, 2018, which is expected to decrease by 30

per cent by the end of the financial year. Assuming that other conditions of relevant Ind AS for applicability

of the impairment are satisfied:

(i) What should be the carrying amount of this machine as at 31st March, 2019?

(ii) How much will be the amount of write off (impairment loss) for the financial year ended 31st March,

2019?

(iii) If the machine had been revalued ten years ago and the current revaluation reserves against this plant

were to be Rs48 lakh, how would you answer the questions in (i) and (ii) above?

10. 16