Page 14 - 10. COMPILER QB - INDAS 36

P. 14

MTPs QUESTIONS

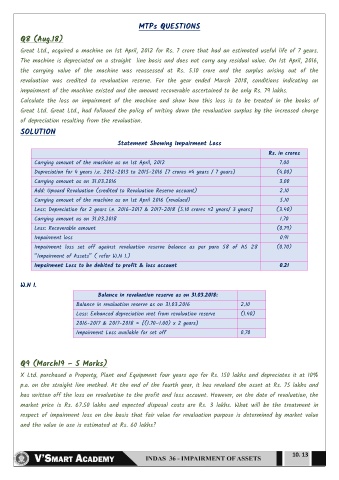

Q8 (Aug.18)

Great Ltd., acquired a machine on 1st April, 2012 for Rs. 7 crore that had an estimated useful life of 7 years.

The machine is depreciated on a straight line basis and does not carry any residual value. On 1st April, 2016,

the carrying value of the machine was reassessed at Rs. 5.10 crore and the surplus arising out of the

revaluation was credited to revaluation reserve. For the year ended March 2018, conditions indicating an

impairment of the machine existed and the amount recoverable ascertained to be only Rs. 79 lakhs.

Calculate the loss on impairment of the machine and show how this loss is to be treated in the books of

Great Ltd. Great Ltd., had followed the policy of writing down the revaluation surplus by the increased charge

of depreciation resulting from the revaluation.

SOLUTION

Statement Showing Impairment Loss

Rs. in crores

Carrying amount of the machine as on 1st April, 2012 7.00

Depreciation for 4 years i.e. 2012-2013 to 2015-2016 [7 crores ×4 years / 7 years] (4.00)

Carrying amount as on 31.03.2016 3.00

Add: Upward Revaluation (credited to Revaluation Reserve account) 2.10

Carrying amount of the machine as on 1st April 2016 (revalued) 5.10

Less: Depreciation for 2 years i.e. 2016-2017 & 2017-2018 [5.10 crores ×2 years/ 3 years] (3.40)

Carrying amount as on 31.03.2018 1.70

Less: Recoverable amount (0.79)

Impairment loss 0.91

Impairment loss set off against revaluation reserve balance as per para 58 of AS 28 (0.70)

“Impairment of Assets” ( refer W.N 1.)

Impairment Loss to be debited to profit & loss account 0.21

W.N 1.

Balance in revaluation reserve as on 31.03.2018:

Balance in revaluation reserve as on 31.03.2016 2.10

Less: Enhanced depreciation met from revaluation reserve (1.40)

2016-2017 & 2017-2018 = [(1.70–1.00) x 2 years]

Impairment Loss available for set off 0.70

Q9 (March19 – 5 Marks)

X Ltd. purchased a Property, Plant and Equipment four years ago for Rs. 150 lakhs and depreciates it at 10%

p.a. on the straight line method. At the end of the fourth year, it has revalued the asset at Rs. 75 lakhs and

has written off the loss on revaluation to the profit and loss account. However, on the date of revaluation, the

market price is Rs. 67.50 lakhs and expected disposal costs are Rs. 3 lakhs. What will be the treatment in

respect of impairment loss on the basis that fair value for revaluation purpose is determined by market value

and the value in use is estimated at Rs. 60 lakhs?

10. 13