Page 13 - 10. COMPILER QB - INDAS 36

P. 13

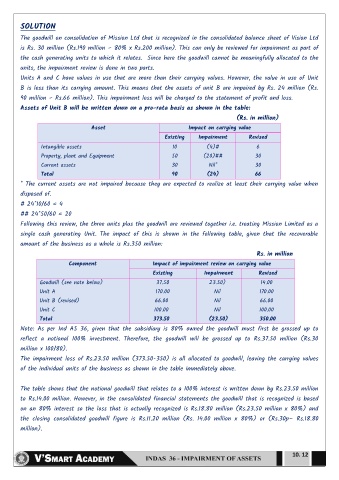

SOLUTION

The goodwill on consolidation of Mission Ltd that is recognized in the consolidated balance sheet of Vision Ltd

is Rs. 30 million (Rs.190 million – 80% x Rs.200 million). This can only be reviewed for impairment as part of

the cash generating units to which it relates. Since here the goodwill cannot be meaningfully allocated to the

units, the impairment review is done in two parts.

Units A and C have values in use that are more than their carrying values. However, the value in use of Unit

B is less than its carrying amount. This means that the assets of unit B are impaired by Rs. 24 million (Rs.

90 million – Rs.66 million). This impairment loss will be charged to the statement of profit and loss.

Assets of Unit B will be written down on a pro-rata basis as shown in the table:

(Rs. in million)

Asset Impact on carrying value

Existing Impairment Revised

Intangible assets 10 (4)# 6

Property, plant and Equipment 50 (20)## 30

Current assets 30 Nil* 30

Total 90 (24) 66

* The current assets are not impaired because they are expected to realize at least their carrying value when

disposed of.

# 24*10/60 = 4

## 24*50/60 = 20

Following this review, the three units plus the goodwill are reviewed together i.e. treating Mission Limited as a

single cash generating Unit. The impact of this is shown in the following table, given that the recoverable

amount of the business as a whole is Rs.350 million:

Rs. in million

Component Impact of impairment review on carrying value

Existing Impairment Revised

Goodwill (see note below) 37.50 23.50) 14.00

Unit A 170.00 Nil 170.00

Unit B (revised) 66.00 Nil 66.00

Unit C 100.00 Nil 100.00

Total 373.50 (23.50) 350.00

Note: As per Ind AS 36, given that the subsidiary is 80% owned the goodwill must first be grossed up to

reflect a notional 100% investment. Therefore, the goodwill will be grossed up to Rs.37.50 million (Rs.30

million x 100/80).

The impairment loss of Rs.23.50 million (373.50-350) is all allocated to goodwill, leaving the carrying values

of the individual units of the business as shown in the table immediately above.

The table shows that the notional goodwill that relates to a 100% interest is written down by Rs.23.50 million

to Rs.14.00 million. However, in the consolidated financial statements the goodwill that is recognized is based

on an 80% interest so the loss that is actually recognized is Rs.18.80 million (Rs.23.50 million x 80%) and

the closing consolidated goodwill figure is Rs.11.20 million (Rs. 14.00 million x 80%) or (Rs.30p– Rs.18.80

million).

10. 12