Page 18 - 3. COMPILER QB - INDAS 16

P. 18

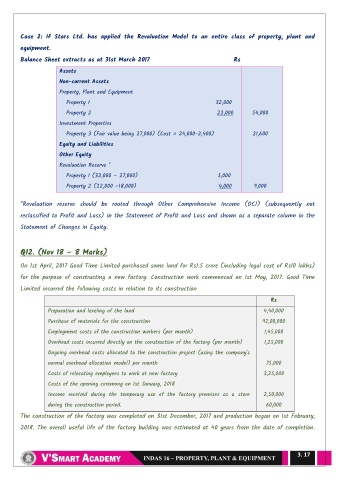

Case 2: If Stars Ltd. has applied the Revaluation Model to an entire class of property, plant and

equipment.

Balance Sheet extracts as at 31st March 2017 Rs

Assets

Non-current Assets

Property, Plant and Equipment

Property 1 32,000

Property 2 22,000 54,000

Investment Properties

Property 3 (Fair value being 27,000) (Cost = 24,000-2,400) 21,600

Equity and Liabilities

Other Equity

Revaluation Reserve *

Property 1 (32,000 – 27,000) 5,000

Property 2 (22,000 –18,000) 4,000 9,000

*Revaluation reserve should be routed through Other Comprehensive Income (OCI) (subsequently not

reclassified to Profit and Loss) in the Statement of Profit and Loss and shown as a separate column in the

Statement of Changes in Equity.

Q12. (Nov 18 – 8 Marks)

On 1st April, 2017 Good Time Limited purchased some land for Rs1.5 crore (including legal cost of Rs10 lakhs)

for the purpose of constructing a new factory. Construction work commenced on 1st May, 2017. Good Time

Limited incurred the following costs in relation to its construction

Rs

Preparation and leveling of the land 4,40,000

Purchase of materials for the construction 92,00,000

Employment costs of the construction workers (per month) 1,45,000

Overhead costs incurred directly on the construction of the factory (per month) 1,25,000

Ongoing overhead costs allocated to the construction project (using the company's

normal overhead allocation model) per month 75,000

Costs of relocating employees to work at new factory 3,25,000

Costs of the opening ceremony on 1st January, 2018

Income received during the temporary use of the factory premises as a store 2,50,000

during the construction period. 60,000

The construction of the factory was completed on 31st December, 2017 and production began on 1st February,

2018. The overall useful life of the factory building was estimated at 40 years from the date of completion.

3. 17