Page 17 - 3. COMPILER QB - INDAS 16

P. 17

However, for investment property, Ind AS 40 states that an entity shall adopt as its accounting policy

the cost model to all of its investment property. Ind AS 40 also requires that an entity shall disclose the

fair value of investment property.

Since property 1 and 2 are used as factory buildings, they should be classified under same category or

class i.e. ―Factory building‖. Therefore, both the properties should be valued either at cost model or

revaluation model.

Hence, the valuation model adopted by Stars Ltd. is not consistent and correct as per Ind AS 16.

In respect to property 3 being classified as Investment Property, there is no alternative of revaluation

model i.e. only cost model is permitted for subsequent measurement. However, Stars Ltd. is required to

disclose the fair value of the investment property in the Notes to Accounts.

(iii) For changes in value on account of revaluation and treatment thereof

Ind AS 16 states that if an asset‖s carrying amount is increased as a result of a revaluation, the increase

shall be recognised in other comprehensive income and accumulated in equity under the heading

―revaluation surplus‖. However, the increase shall be recognised in profit or loss to the extent that it

reverses a revaluation decrease of the same asset previously recognised in profit or loss. Accordingly, the

revaluation gain shall be recognised in other comprehensive income and accumulated in equity under the

heading of revaluation surplus.

(iv) For treatment of depreciation

Ind AS 16 states that depreciation is recognised even if the fair value of the asset exceeds its carrying

amount, as long as the asset‖s residual value does not exceed its carrying amount. Accordingly, Stars Ltd.

is required to depreciate these properties irrespective of the fact that their fair value exceeds the

carrying amount.

(v) Rectified presentation in the balance sheet

As per the provisions of Ind AS 1, Ind AS 16 and Ind AS 40, the presentation of these three properties in

the balance sheet should be as follows:

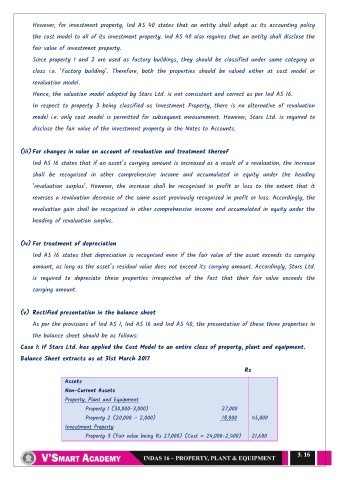

Case 1: If Stars Ltd. has applied the Cost Model to an entire class of property, plant and equipment.

Balance Sheet extracts as at 31st March 2017

Rs

Assets

Non-Current Assets

Property, Plant and Equipment

Property 1 (30,000-3,000) 27,000

Property 2 (20,000 – 2,000) 18,000 45,000

Investment Property

Property 3 (Fair value being Rs 27,000) (Cost = 24,000-2,400) 21,600

3. 16