Page 13 - 3. COMPILER QB - INDAS 16

P. 13

st

Carrying value of production line as on 31 March, 20X2:

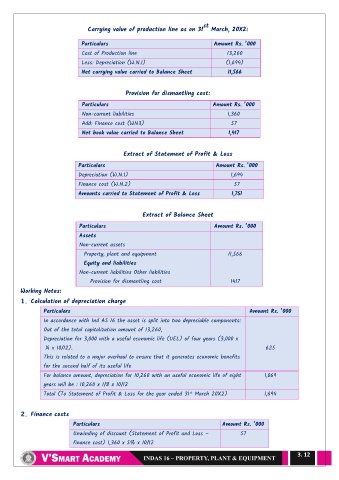

Particulars Amount Rs. ’000

Cost of Production line 13,260

Less: Depreciation (W.N.1) (1,694)

Net carrying value carried to Balance Sheet 11,566

Provision for dismantling cost:

Particulars Amount Rs. ’000

Non-current liabilities 1,360

Add: Finance cost (WN3) 57

Net book value carried to Balance Sheet 1,417

Extract of Statement of Profit & Loss

Particulars Amount Rs. ’000

Depreciation (W.N.1) 1,694

Finance cost (W.N.2) 57

Amounts carried to Statement of Profit & Loss 1,751

Extract of Balance Sheet

Particulars Amount Rs. ’000

Assets

Non-current assets

Property, plant and equipment 11,566

Equity and liabilities

Non-current liabilities Other liabilities

Provision for dismantling cost 1417

Working Notes:

1. Calculation of depreciation charge

Particulars Amount Rs. ’000

In accordance with Ind AS 16 the asset is split into two depreciable components:

Out of the total capitalization amount of 13,260,

Depreciation for 3,000 with a useful economic life (UEL) of four years (3,000 x

¼ x 10/12). 625

This is related to a major overhaul to ensure that it generates economic benefits

for the second half of its useful life

For balance amount, depreciation for 10,260 with an useful economic life of eight 1,069

years will be : 10,260 x 1/8 x 10/12

st

Total (To Statement of Profit & Loss for the year ended 31 March 20X2) 1,694

2. Finance costs

Particulars Amount Rs. ’000

Unwinding of discount (Statement of Profit and Loss – 57

finance cost) 1,360 x 5% x 10/12

3. 12