Page 49 - 16. COMPILER QB - INDAS 103

P. 49

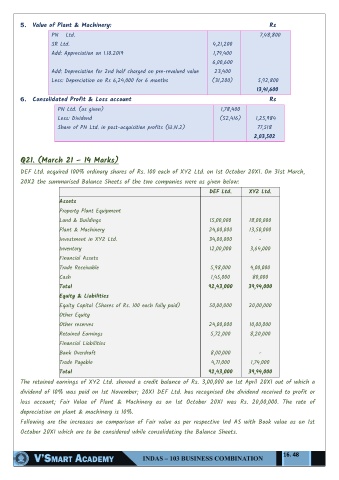

5. Value of Plant & Machinery: Rs

PN Ltd. 7,48,800

SR Ltd. 4,21,200

Add: Appreciation on 1.10.2019 1,79,400

6,00,600

Add: Depreciation for 2nd half charged on pre-revalued value 23,400

Less: Depreciation on Rs 6,24,000 for 6 months (31,200) 5,92,800

13,41,600

6. Consolidated Profit & Loss account Rs

PN Ltd. (as given) 1,78,400

Less: Dividend (52,416) 1,25,984

Share of PN Ltd. in post-acquisition profits (W.N.2) 77,518

2,03,502

Q21. (March 21 – 14 Marks)

DEF Ltd. acquired 100% ordinary shares of Rs. 100 each of XYZ Ltd. on 1st October 20X1. On 31st March,

20X2 the summarised Balance Sheets of the two companies were as given below:

DEF Ltd. XYZ Ltd.

Assets

Property Plant Equipment

Land & Buildings 15,00,000 18,00,000

Plant & Machinery 24,00,000 13,50,000

Investment in XYZ Ltd. 34,00,000 -

Inventory 12,00,000 3,64,000

Financial Assets

Trade Receivable 5,98,000 4,00,000

Cash 1,45,000 80,000

Total 92,43,000 39,94,000

Equity & Liabilities

Equity Capital (Shares of Rs. 100 each fully paid) 50,00,000 20,00,000

Other Equity

Other reserves 24,00,000 10,00,000

Retained Earnings 5,72,000 8,20,000

Financial Liabilities

Bank Overdraft 8,00,000 -

Trade Payable 4,71,000 1,74,000

Total 92,43,000 39,94,000

The retained earnings of XYZ Ltd. showed a credit balance of Rs. 3,00,000 on 1st April 20X1 out of which a

dividend of 10% was paid on 1st November; 20X1 DEF Ltd. has recognised the dividend received to profit or

loss account; Fair Value of Plant & Machinery as on 1st October 20X1 was Rs. 20,00,000. The rate of

depreciation on plant & machinery is 10%.

Following are the increases on comparison of Fair value as per respective Ind AS with Book value as on 1st

October 20X1 which are to be considered while consolidating the Balance Sheets.

16. 48