Page 52 - 16. COMPILER QB - INDAS 103

P. 52

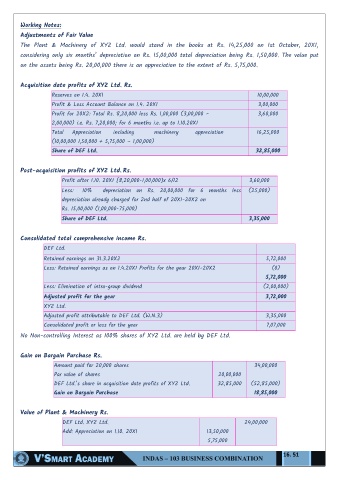

Working Notes:

Adjustments of Fair Value

The Plant & Machinery of XYZ Ltd. would stand in the books at Rs. 14,25,000 on 1st October, 20X1,

considering only six months‖ depreciation on Rs. 15,00,000 total depreciation being Rs. 1,50,000. The value put

on the assets being Rs. 20,00,000 there is an appreciation to the extent of Rs. 5,75,000.

Acquisition date profits of XYZ Ltd. Rs.

Reserves on 1.4. 20X1 10,00,000

Profit & Loss Account Balance on 1.4. 20X1 3,00,000

Profit for 20X2: Total Rs. 8,20,000 less Rs. 1,00,000 (3,00,000 – 3,60,000

2,00,000) i.e. Rs. 7,20,000; for 6 months i.e. up to 1.10.20X1

Total Appreciation including machinery appreciation 16,25,000

(10,00,000 1,50,000 + 5,75,000 – 1,00,000)

Share of DEF Ltd. 32,85,000

Post-acquisition profits of XYZ Ltd. Rs.

Profit after 1.10. 20X1 [8,20,000-1,00,000]x 6/12 3,60,000

Less: 10% depreciation on Rs. 20,00,000 for 6 months less (25,000)

depreciation already charged for 2nd half of 20X1-20X2 on

Rs. 15,00,000 (1,00,000-75,000)

Share of DEF Ltd. 3,35,000

Consolidated total comprehensive income Rs.

DEF Ltd.

Retained earnings on 31.3.20X2 5,72,000

Less: Retained earnings as on 1.4.20X1 Profits for the year 20X1-20X2 (0)

5,72,000

Less: Elimination of intra-group dividend (2,00,000)

Adjusted profit for the year 3,72,000

XYZ Ltd.

Adjusted profit attributable to DEF Ltd. (W.N.3) 3,35,000

Consolidated profit or loss for the year 7,07,000

No Non-controlling Interest as 100% shares of XYZ Ltd. are held by DEF Ltd.

Gain on Bargain Purchase Rs.

Amount paid for 20,000 shares 34,00,000

Par value of shares 20,00,000

DEF Ltd.‖s share in acquisition date profits of XYZ Ltd. 32,85,000 (52,85,000)

Gain on Bargain Purchase 18,85,000

Value of Plant & Machinery Rs.

DEF Ltd. XYZ Ltd. 24,00,000

Add: Appreciation on 1.10. 20X1 13,50,000

5,75,000

16. 51