Page 14 - 20. COMPILER QB - INDAS 102

P. 14

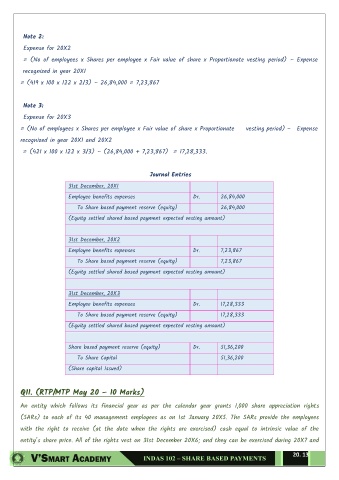

Note 2:

Expense for 20X2

= (No of employees x Shares per employee x Fair value of share x Proportionate vesting period) – Expense

recognized in year 20X1

= (419 x 100 x 122 x 2/3) – 26,84,000 = 7,23,867

Note 3:

Expense for 20X3

= (No of employees x Shares per employee x Fair value of share x Proportionate vesting period) – Expense

recognized in year 20X1 and 20X2

= (421 x 100 x 122 x 3/3) – (26,84,000 + 7,23,867) = 17,28,333.

Journal Entries

31st December, 20X1

Employee benefits expenses Dr. 26,84,000

To Share based payment reserve (equity) 26,84,000

(Equity settled shared based payment expected vesting amount)

31st December, 20X2

Employee benefits expenses Dr. 7,23,867

To Share based payment reserve (equity) 7,23,867

(Equity settled shared based payment expected vesting amount)

31st December, 20X3

Employee benefits expenses Dr. 17,28,333

To Share based payment reserve (equity) 17,28,333

(Equity settled shared based payment expected vesting amount)

Share based payment reserve (equity) Dr. 51,36,200

To Share Capital 51,36,200

(Share capital Issued)

Q11. (RTP/MTP May 20 – 10 Marks)

An entity which follows its financial year as per the calendar year grants 1,000 share appreciation rights

(SARs) to each of its 40 management employees as on 1st January 20X5. The SARs provide the employees

with the right to receive (at the date when the rights are exercised) cash equal to intrinsic value of the

entity’s share price. All of the rights vest on 31st December 20X6; and they can be exercised during 20X7 and

20. 13