Page 18 - 20. COMPILER QB - INDAS 102

P. 18

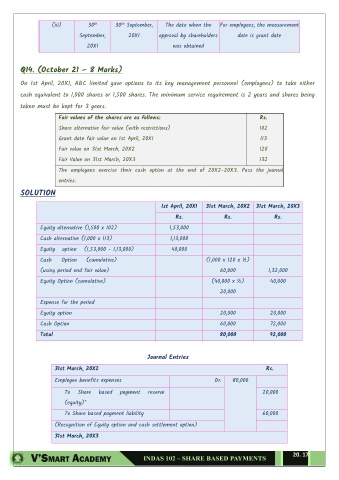

(iii) 30 30 September, The date when the For employees, the measurement

th

th

September, 20X1 approval by shareholders date is grant date

20X1 was obtained

Q14. (October 21 – 8 Marks)

On 1st April, 20X1, ABC limited gave options to its key management personnel (employees) to take either

cash equivalent to 1,000 shares or 1,500 shares. The minimum service requirement is 2 years and shares being

taken must be kept for 3 years.

Fair values of the shares are as follows: Rs.

Share alternative fair value (with restrictions) 102

Grant date fair value on 1st April, 20X1 113

Fair value on 31st March, 20X2 120

Fair Value on 31st March, 20X3 132

The employees exercise their cash option at the end of 20X2-20X3. Pass the journal

entries.

SOLUTION

1st April, 20X1 31st March, 20X2 31st March, 20X3

Rs. Rs. Rs.

Equity alternative (1,500 x 102) 1,53,000

Cash alternative (1,000 x 113) 1,13,000

Equity option (1,53,000 - 1,13,000) 40,000

Cash Option (cumulative) (1,000 x 120 x ½)

(using period end fair value) 60,000 1,32,000

Equity Option (cumulative) (40,000 x ½) 40,000

20,000

Expense for the period

Equity option 20,000 20,000

Cash Option 60,000 72,000

Total 80,000 92,000

Journal Entries

31st March, 20X2 Rs.

Employee benefits expenses Dr. 80,000

To Share based payment reserve 20,000

(equity)*

To Share based payment liability 60,000

(Recognition of Equity option and cash settlement option)

31st March, 20X3

20. 17