Page 23 - 20. COMPILER QB - INDAS 102

P. 23

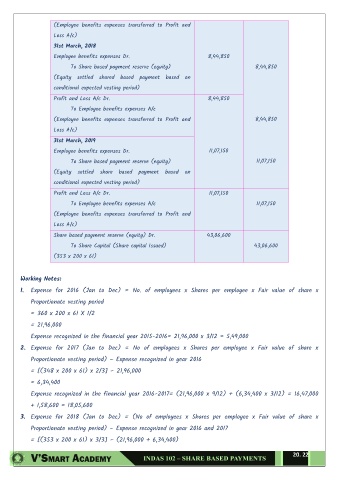

(Employee benefits expenses transferred to Profit and

Loss A/c)

31st March, 2018

Employee benefits expenses Dr. 8,44,850

To Share based payment reserve (equity) 8,44,850

(Equity settled shared based payment based on

conditional expected vesting period)

Profit and Loss A/c Dr. 8,44,850

To Employee benefits expenses A/c

(Employee benefits expenses transferred to Profit and 8,44,850

Loss A/c)

31st March, 2019

Employee benefits expenses Dr. 11,07,150

To Share based payment reserve (equity) 11,07,150

(Equity settled share based payment based on

conditional expected vesting period)

Profit and Loss A/c Dr. 11,07,150

To Employee benefits expenses A/c 11,07,150

(Employee benefits expenses transferred to Profit and

Loss A/c)

Share based payment reserve (equity) Dr. 43,06,600

To Share Capital (Share capital Issued) 43,06,600

(353 x 200 x 61)

Working Notes:

1. Expense for 2016 (Jan to Dec) = No. of employees x Shares per employee x Fair value of share x

Proportionate vesting period

= 360 x 200 x 61 X 1/2

= 21,96,000

Expense recognized in the financial year 2015-2016= 21,96,000 x 3/12 = 5,49,000

2. Expense for 2017 (Jan to Dec) = No of employees x Shares per employee x Fair value of share x

Proportionate vesting period) – Expense recognized in year 2016

= [(348 x 200 x 61) x 2/3] – 21,96,000

= 6,34,400

Expense recognized in the financial year 2016-2017= (21,96,000 x 9/12) + (6,34,400 x 3/12) = 16,47,000

+ 1,58,600 = 18,05,600

3. Expense for 2018 (Jan to Dec) = (No of employees x Shares per employee x Fair value of share x

Proportionate vesting period) – Expense recognized in year 2016 and 2017

= [(353 x 200 x 61) x 3/3] – (21,96,000 + 6,34,400)

20. 22