Page 22 - 20. COMPILER QB - INDAS 102

P. 22

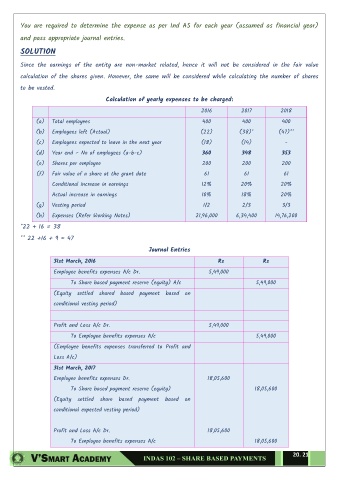

You are required to determine the expense as per Ind AS for each year (assumed as financial year)

and pass appropriate journal entries.

SOLUTION

Since the earnings of the entity are non-market related, hence it will not be considered in the fair value

calculation of the shares given. However, the same will be considered while calculating the number of shares

to be vested.

Calculation of yearly expenses to be charged:

2016 2017 2018

(a) Total employees 400 400 400

(b) Employees left (Actual) (22) (38)* (47)**

(c) Employees expected to leave in the next year (18) (14) -

(d) Year end – No of employees (a-b-c) 360 348 353

(e) Shares per employee 200 200 200

(f) Fair value of a share at the grant date 61 61 61

Conditional increase in earnings 12% 20% 20%

Actual increase in earnings 10% 18% 20%

(g) Vesting period 1/2 2/3 3/3

(h) Expenses (Refer Working Notes) 21,96,000 6,34,400 14,76,200

*22 + 16 = 38

** 22 +16 + 9 = 47

Journal Entries

31st March, 2016 Rs Rs

Employee benefits expenses A/c Dr. 5,49,000

To Share based payment reserve (equity) A/c 5,49,000

(Equity settled shared based payment based on

conditional vesting period)

Profit and Loss A/c Dr. 5,49,000

To Employee benefits expenses A/c 5,49,000

(Employee benefits expenses transferred to Profit and

Loss A/c)

31st March, 2017

Employee benefits expenses Dr. 18,05,600

To Share based payment reserve (equity) 18,05,600

(Equity settled share based payment based on

conditional expected vesting period)

Profit and Loss A/c Dr. 18,05,600

To Employee benefits expenses A/c 18,05,600

20. 21