Page 21 - 20. COMPILER QB - INDAS 102

P. 21

st

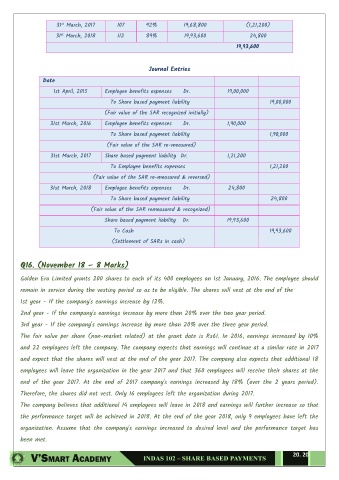

31 March, 2017 107 92% 19,68,800 (1,21,200)

st

31 March, 2018 112 89% 19,93,600 24,800

19,93,600

Journal Entries

Date

1st April, 2015 Employee benefits expenses Dr. 19,00,000

To Share based payment liability 19,00,000

(Fair value of the SAR recognized initially)

31st March, 2016 Employee benefits expenses Dr. 1,90,000

To Share based payment liability 1,90,000

(Fair value of the SAR re-measured)

31st March, 2017 Share based payment liability Dr. 1,21,200

To Employee benefits expenses 1,21,200

(Fair value of the SAR re-measured & reversed)

31st March, 2018 Employee benefits expenses Dr. 24,800

To Share based payment liability 24,800

(Fair value of the SAR remeasured & recognized)

Share based payment liability Dr. 19,93,600

To Cash 19,93,600

(Settlement of SARs in cash)

Q16. (November 18 – 8 Marks)

Golden Era Limited grants 200 shares to each of its 400 employees on 1st January, 2016. The employee should

remain in service during the vesting period so as to be eligible. The shares will vest at the end of the

1st year - If the company's earnings increase by 12%.

2nd year - If the company's earnings increase by more than 20% over the two year period.

3rd year - If the company's earnings increase by more than 20% over the three year period.

The fair value per share (non-market related) at the grant date is Rs61. In 2016, earnings increased by 10%

and 22 employees left the company. The company expects that earnings will continue at a similar rate in 2017

and expect that the shares will vest at the end of the year 2017. The company also expects that additional 18

employees will leave the organization in the year 2017 and that 360 employees will receive their shares at the

end of the year 2017. At the end of 2017 company's earnings increased by 18% (over the 2 years period).

Therefore, the shares did not vest. Only 16 employees left the organization during 2017.

The company believes that additional 14 employees will leave in 2018 and earnings will further increase so that

the performance target will be achieved in 2018. At the end of the year 2018, only 9 employees have left the

organization. Assume that the company's earnings increased to desired level and the performance target has

been met.

20. 20