Page 9 - 21. COMPILER QB - INDAS 33

P. 9

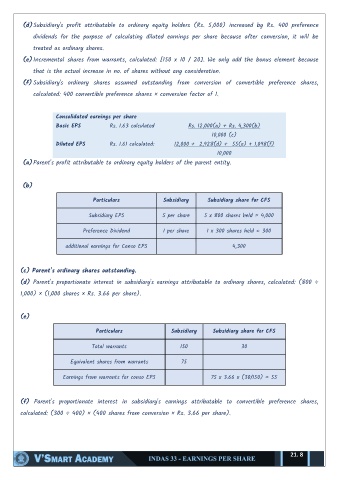

(d) Subsidiary's profit attributable to ordinary equity holders (Rs. 5,000) increased by Rs. 400 preference

dividends for the purpose of calculating diluted earnings per share because after conversion, it will be

treated as ordinary shares.

(e) Incremental shares from warrants, calculated: [150 x 10 / 20]. We only add the bonus element because

that is the actual increase in no. of shares without any consideration.

(f) Subsidiary's ordinary shares assumed outstanding from conversion of convertible preference shares,

calculated: 400 convertible preference shares × conversion factor of 1.

Consolidated earnings per share

Basic EPS Rs. 1.63 calculated Rs. 12,000(a) + Rs. 4,300(b)

10,000 (c)

Diluted EPS Rs. 1.61 calculated: 12,000 + 2,928(d) + 55(e) + 1,098(f)

10,000

(a) Parent's profit attributable to ordinary equity holders of the parent entity.

(b)

Particulars Subsidiary Subsidiary share for CFS

Subsidiary EPS 5 per share 5 x 800 shares held = 4,000

Preference Dividend 1 per share 1 x 300 shares held = 300

additional earnings for Conso EPS 4,300

(c) Parent's ordinary shares outstanding.

(d) Parent's proportionate interest in subsidiary's earnings attributable to ordinary shares, calculated: (800 ÷

1,000) × (1,000 shares × Rs. 3.66 per share).

(e)

Particulars Subsidiary Subsidiary share for CFS

Total warrants 150 30

Equivalent shares from warrants 75

Earnings from warrants for conso EPS 75 x 3.66 x (30/150) = 55

(f) Parent's proportionate interest in subsidiary's earnings attributable to convertible preference shares,

calculated: (300 ÷ 400) × (400 shares from conversion × Rs. 3.66 per share).

21. 8