Page 6 - 21. COMPILER QB - INDAS 33

P. 6

* Note- if debentures are converted to equity shares, then the interest will not be payable. This saving of

interest payment will be available for equity holders. However, tax will be paid on this amount.

Weighted average number of shares = 20,00,00,000 + {5,00,00,000 x (9/12)} + 10,00,00,000 = 33,75,00,000

shares or 3,37,500 thousand shares

Diluted EPS = Rs 45,299.83 thousand / 3,37,500 thousand shares = Rs 0.134

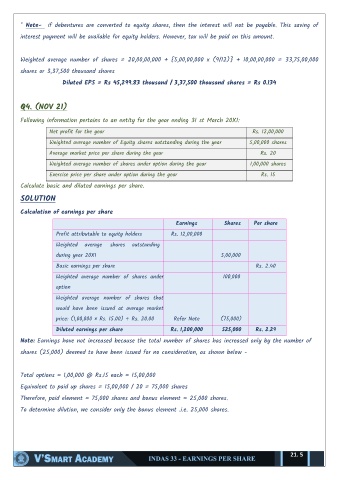

Q4. (NOV 21)

Following information pertains to an entity for the year ending 31 st March 20X1:

Net profit for the year Rs. 12,00,000

Weighted average number of Equity shares outstanding during the year 5,00,000 shares

Average market price per share during the year Rs. 20

Weighted average number of shares under option during the year 1,00,000 shares

Exercise price per share under option during the year Rs. 15

Calculate basic and diluted earnings per share.

SOLUTION

Calculation of earnings per share

Earnings Shares Per share

Profit attributable to equity holders Rs. 12,00,000

Weighted average shares outstanding

during year 20X1 5,00,000

Basic earnings per share Rs. 2.40

Weighted average number of shares under 100,000

option

Weighted average number of shares that

would have been issued at average market

price: (1,00,000 × Rs. 15.00) ÷ Rs. 20.00 Refer Note (75,000)

Diluted earnings per share Rs. 1,200,000 525,000 Rs. 2.29

Note: Earnings have not increased because the total number of shares has increased only by the number of

shares (25,000) deemed to have been issued for no consideration, as shown below -

Total options = 1,00,000 @ Rs.15 each = 15,00,000

Equivalent to paid up shares = 15,00,000 / 20 = 75,000 shares

Therefore, paid element = 75,000 shares and bonus element = 25,000 shares.

To determine dilution, we consider only the bonus element .i.e. 25,000 shares.

21. 5