Page 41 - 23. COMPILER QB - IND AS 109_32

P. 41

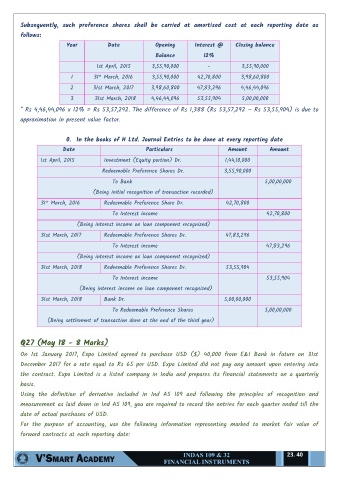

Subsequently, such preference shares shall be carried at amortised cost at each reporting date as

follows:

Year Date Opening Interest @ Closing balance

Balance 12%

1st April, 2015 3,55,90,000 - 3,55,90,000

st

1 31 March, 2016 3,55,90,000 42,70,800 3,98,60,800

2 31st March, 2017 3,98,60,800 47,83,296 4,46,44,096

3 31st March, 2018 4,46,44,096 53,55,904 5,00,00,000

* Rs 4,46,44,096 x 12% = Rs 53,57,292. The difference of Rs 1,388 (Rs 53,57,292 – Rs 53,55,904) is due to

approximation in present value factor.

0. In the books of H Ltd. Journal Entries to be done at every reporting date

Date Particulars Amount Amount

1st April, 2015 Investment (Equity portion) Dr. 1,44,10,000

Redeemable Preference Shares Dr. 3,55,90,000

To Bank 5,00,00,000

(Being initial recognition of transaction recorded)

st

31 March, 2016 Redeemable Preference Share Dr. 42,70,800

To Interest income 42,70,800

(Being interest income on loan component recognized)

31st March, 2017 Redeemable Preference Shares Dr. 47,83,296

To Interest income 47,83,296

(Being interest income on loan component recognized)

31st March, 2018 Redeemable Preference Shares Dr. 53,55,904

To Interest income 53,55,904

(Being interest income on loan component recognized)

31st March, 2018 Bank Dr. 5,00,00,000

To Redeemable Preference Shares 5,00,00,000

(Being settlement of transaction done at the end of the third year)

Q27 (May 18 - 8 Marks)

On 1st January 2017, Expo Limited agreed to purchase USD ($) 40,000 from E&I Bank in future on 31st

December 2017 for a rate equal to Rs 65 per USD. Expo Limited did not pay any amount upon entering into

the contract. Expo Limited is a listed company in India and prepares its financial statements on a quarterly

basis.

Using the definition of derivative included in Ind AS 109 and following the principles of recognition and

measurement as laid down in Ind AS 109, you are required to record the entries for each quarter ended till the

date of actual purchases of USD.

For the purpose of accounting, use the following information representing marked to market fair value of

forward contracts at each reporting date:

23. 40