Page 45 - 23. COMPILER QB - IND AS 109_32

P. 45

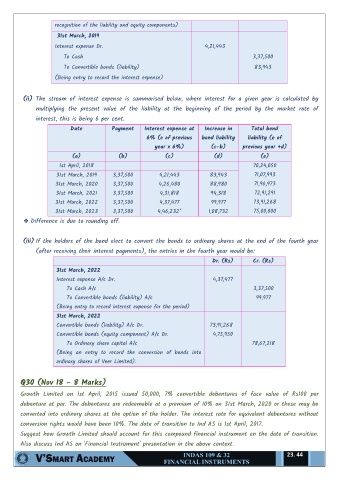

recognition of the liability and equity components)

31st March, 2019

Interest expense Dr. 4,21,443

To Cash 3,37,500

To Convertible bonds (liability) 83,943

(Being entry to record the interest expense)

(ii) The stream of interest expense is summarised below, where interest for a given year is calculated by

multiplying the present value of the liability at the beginning of the period by the market rate of

interest, this is being 6 per cent.

Date Payment Interest expense at Increase in Total bond

6% (e of previous bond liability liability (e of

year x 6%) (c-b) previous year +d)

(a) (b) (c) (d) (e)

1st April, 2018 70,24,050

31st March, 2019 3,37,500 4,21,443 83,943 71,07,993

31st March, 2020 3,37,500 4,26,480 88,980 71,96,973

31st March, 2021 3,37,500 4,31,818 94,318 72,91,291

31st March, 2022 3,37,500 4,37,477 99,977 73,91,268

31st March, 2023 3,37,500 4,46,232* 1,08,732 75,00,000

❖ Difference is due to rounding off.

(iii) If the holders of the bond elect to convert the bonds to ordinary shares at the end of the fourth year

(after receiving their interest payments), the entries in the fourth year would be:

Dr. (Rs) Cr. (Rs)

31st March, 2022

Interest expense A/c Dr. 4,37,477

To Cash A/c 3,37,500

To Convertible bonds (liability) A/c 99,977

(Being entry to record interest expense for the period)

31st March, 2022

Convertible bonds (liability) A/c Dr. 73,91,268

Convertible bonds (equity component) A/c Dr. 4,75,950

To Ordinary share capital A/c 78,67,218

(Being an entry to record the conversion of bonds into

ordinary shares of Veer Limited).

Q30 (Nov 18 - 8 Marks)

Growth Limited on 1st April, 2015 issued 50,000, 7% convertible debentures of face value of Rs100 per

debenture at par. The debentures are redeemable at a premium of 10% on 31st March, 2020 or these may be

converted into ordinary shares at the option of the holder. The interest rate for equivalent debentures without

conversion rights would have been 10%. The date of transition to Ind AS is 1st April, 2017.

Suggest how Growth Limited should account for this compound financial instrument on the date of transition.

Also discuss Ind AS on 'Financial Instrument' presentation in the above context.

23. 44