Page 42 - 23. COMPILER QB - IND AS 109_32

P. 42

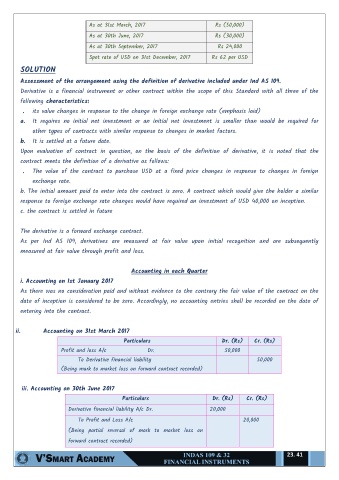

As at 31st March, 2017 Rs (50,000)

As at 30th June, 2017 Rs (30,000)

As at 30th September, 2017 Rs 24,000

Spot rate of USD on 31st December, 2017 Rs 62 per USD

SOLUTION

Assessment of the arrangement using the definition of derivative included under Ind AS 109.

Derivative is a financial instrument or other contract within the scope of this Standard with all three of the

following characteristics:

. its value changes in response to the change in foreign exchange rate (emphasis laid)

a. It requires no initial net investment or an initial net investment is smaller than would be required for

other types of contracts with similar response to changes in market factors.

b. It is settled at a future date.

Upon evaluation of contract in question, on the basis of the definition of derivative, it is noted that the

contract meets the definition of a derivative as follows:

. The value of the contract to purchase USD at a fixed price changes in response to changes in foreign

exchange rate.

b. The initial amount paid to enter into the contract is zero. A contract which would give the holder a similar

response to foreign exchange rate changes would have required an investment of USD 40,000 on inception.

c. the contract is settled in future

The derivative is a forward exchange contract.

As per Ind AS 109, derivatives are measured at fair value upon initial recognition and are subsequently

measured at fair value through profit and loss.

Accounting in each Quarter

i. Accounting on 1st January 2017

As there was no consideration paid and without evidence to the contrary the fair value of the contract on the

date of inception is considered to be zero. Accordingly, no accounting entries shall be recorded on the date of

entering into the contract.

ii. Accounting on 31st March 2017

Particulars Dr. (Rs) Cr. (Rs)

Profit and loss A/c Dr. 50,000

To Derivative financial liability 50,000

(Being mark to market loss on forward contract recorded)

iii. Accounting on 30th June 2017

Particulars Dr. (Rs) Cr. (Rs)

Derivative financial liability A/c Dr. 20,000

To Profit and Loss A/c 20,000

(Being partial reversal of mark to market loss on

forward contract recorded)

23. 41