Page 125 - CA Final PARAM Digital Book.

P. 125

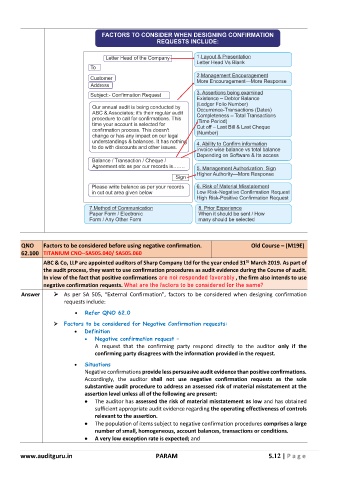

QNO Factors to be considered before using negative confirmation. Old Course – (M19E)

62.100 TITANIUM CNO--SA505.040/ SA505.060

St

ABC & Co, LLP are appointed auditors of Sharp Company Ltd for the year ended 31 March 2019. As part of

the audit process, they want to use confirmation procedures as audit evidence during the Course of audit.

In view of the fact that positive confirmations are not responded favorably , the firm also intends to use

negative confirmation requests. What are the factors to be considered for the same?

Answer ➢ As per SA 505, “External Confirmation”, factors to be considered when designing confirmation

requests include:

• Refer QNO 62.0

➢ Factors to be considered for Negative Confirmation requests:

• Definition

• Negative confirmation request –

A request that the confirming party respond directly to the auditor only if the

confirming party disagrees with the information provided in the request.

• Situations

Negative confirmations provide less persuasive audit evidence than positive confirmations.

Accordingly, the auditor shall not use negative confirmation requests as the sole

substantive audit procedure to address an assessed risk of material misstatement at the

assertion level unless all of the following are present:

• The auditor has assessed the risk of material misstatement as low and has obtained

sufficient appropriate audit evidence regarding the operating effectiveness of controls

relevant to the assertion.

• The population of items subject to negative confirmation procedures comprises a large

number of small, homogeneous, account balances, transactions or conditions.

• A very low exception rate is expected; and

www.auditguru.in PARAM 5.12 | P a g e