Page 29 - Chap7 ITC

P. 29

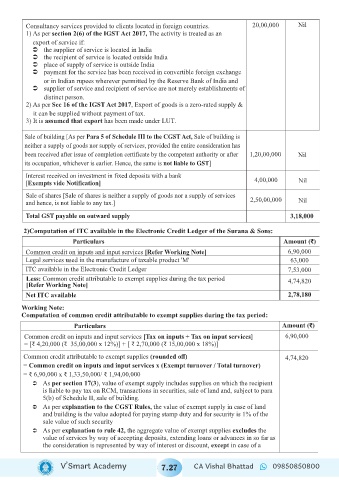

Consultancy services provided to clients located in foreign countries. 20,00,000 Nil

1) As per section 2(6) of the IGST Act 2017, The activity is treated as an

export of service if:

Ü the supplier of service is located in India

Ü the recipient of service is located outside India

Ü place of supply of service is outside India

Ü payment for the service has been received in convertible foreign exchange

or in Indian rupees wherever permitted by the Reserve Bank of India and

Ü supplier of service and recipient of service are not merely establishments of

distinct person.

2) As per Sec 16 of the IGST Act 2017, Export of goods is a zero-rated supply &

it can be supplied without payment of tax.

3) It is assumed that export has been made under LUT.

Sale of building [As per Para 5 of Schedule III to the CGST Act, Sale of building is

neither a supply of goods nor supply of services, provided the entire consideration has

been received after issue of completion certificate by the competent authority or after 1,20,00,000 Nil

its occupation, whichever is earlier. Hence, the same is not liable to GST]

Interest received on investment in fixed deposits with a bank

[Exempts vide Notification] 4,00,000 Nil

Sale of shares [Sale of shares is neither a supply of goods nor a supply of services

and hence, is not liable to any tax.] 2,50,00,000 Nil

Total GST payable on outward supply 3,18,000

2) Computation of ITC available in the Electronic Credit Ledger of the Surana & Sons:

Particulars Amount (₹)

Common credit on inputs and input services [Refer Working Note] 6,90,000

Legal services used in the manufacture of taxable product 'M' 63,000

ITC available in the Electronic Credit Ledger 7,53,000

Less: Common credit attributable to exempt supplies during the tax period 4,74,820

[Refer Working Note]

Net ITC available 2,78,180

Working Note:

Computation of common credit attributable to exempt supplies during the tax period:

Particulars Amount (₹)

Common credit on inputs and input services [Tax on inputs + Tax on input services] 6,90,000

= [₹ 4,20,000 (₹ 35,00,000 x 12%)] + [ ₹ 2,70,000 (₹ 15,00,000 x 18%)]

Common credit attributable to exempt supplies (rounded off) 4,74,820

= Common credit on inputs and input services x (Exempt turnover / Total turnover)

= ₹ 6,90,000 x ₹ 1,33,50,000/ ₹ 1,94,00,000

Ü As per section 17(3), value of exempt supply includes supplies on which the recipient

is liable to pay tax on RCM, transactions in securities, sale of land and, subject to para

5(b) of Schedule II, sale of building.

Ü As per explanation to the CGST Rules, the value of exempt supply in case of land

and building is the value adopted for paying stamp duty and for security is 1% of the

sale value of such security

Ü As per explanation to rule 42, the aggregate value of exempt supplies excludes the

value of services by way of accepting deposits, extending loans or advances in so far as

the consideration is represented by way of interest or discount, except in case of a

V’Smart Academy 7.27 CA Vishal Bhattad 09850850800