Page 31 - Chap7 ITC

P. 31

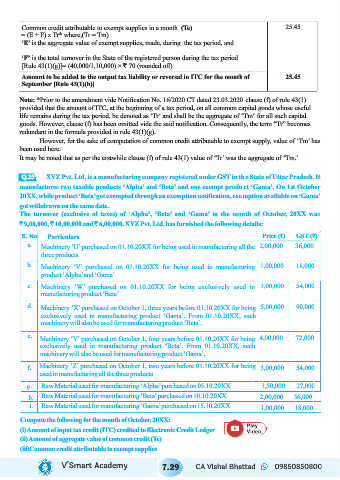

Common credit attributable to exempt supplies in a month (Te) 25.45

= (E ÷ F) x Tr* where,(Tr = Tm)

‘E’ is the aggregate value of exempt supplies, made, during the tax period, and

‘F’ is the total turnover in the State of the registered person during the tax period

[Rule 43(1)(g)]= (40,000/1,10,000) × ` 70 (rounded off)

Amount to be added to the output tax liability or reversal in ITC for the month of 25.45

September [Rule 43(1)(h)]

Note: *Prior to the amendment vide Notification No. 16/2020 CT dated 23.03.2020 clause (f) of rule 43(1)

provided that the amount of ITC, at the beginning of a tax period, on all common capital goods whose useful

life remains during the tax period, be denoted as ‘Tr‘ and shall be the aggregate of ‘Tm‘ for all such capital

goods. However, clause (f) has been omitted vide the said notification. Consequently, the term “Tr” becomes

redundant in the formula provided in rule 43(1)(g).

However, for the sake of computation of common credit attributable to exempt supply, value of ‘Tm’ has

been used here.

It may be noted that as per the erstwhile clause (f) of rule 43(1) value of ‘Tr’ was the aggregate of ‘Tm.’

Q.25

XYZ Pvt. Ltd. is a manufacturing company registered under GST in the State of Uttar Pradesh. It

manufactures two taxable products ‘Alpha’ and ‘Beta’ and one exempt product ‘Gama’. On 1st October

20XX, while product ‘Beta’ got exempted through an exemption notification, exemption available on ‘Gama’

got withdrawn on the same date.

The turnover (exclusive of taxes) of ‘Alpha’, ‘Beta’ and ‘Gama’ in the month of October, 20XX was

` 9,00,000, ` 10,00,000 and ` 6,00,000. XYZ Pvt. Ltd. has furnished the following details:

S. No. Particulars Price (₹) GST (₹)

a. Machinery ‘U’ purchased on 01.10.20XX for being used in manufacturing all the 2,00,000 36,000

three products

b. Machinery ‘V’ purchased on 01.10.20XX for being used in manufacturing 1,00,000 18,000

product ‘Alpha’ and ‘Gama’

c. Machinery ‘W’ purchased on 01.10.20XX for being exclusively used in 3,00,000 54,000

manufacturing product ‘Beta’

d. 5,00,000 90,000

Machinery ‘X’ purchased on October 1, three years before 01.10.20XX for being

exclusively used in manufacturing product ‘Gama’. From 01.10.20XX, such

machinery will also be used for manufacturing product ‘Beta’.

e. 4,00,000 72,000

Machinery ‘Y’ purchased on October 1, four years before 01.10.20XX for being

exclusively used in manufacturing product ‘Beta’. From 01.10.20XX, such

machinery will also be used for manufacturing product ‘Gama’.

f. Machinery ‘Z’ purchased on October 1, two years before 01.10.20XX for being 3,00,000 54,000

used in manufacturing all the three products

g. Raw Material used for manufacturing ‘Alpha’ purchased on 05.10.20XX 1,50,000 27,000

h. Raw Material used for manufacturing ‘Beta’ purchased on 10.10.20XX 2,00,000 36,000

i. Raw Material used for manufacturing ‘Gama’ purchased on 15.10.20XX 1,00,000 18,000

Compute the following for the month of October, 20XX:

(i) Amount of input tax credit (ITC) credited to Electronic Credit Ledger

(ii) Amount of aggregate value of common credit (Tc)

(iii)Common credit attributable to exempt supplies

V’Smart Academy 7.29 CA Vishal Bhattad 09850850800