Page 33 - Chap7 ITC

P. 33

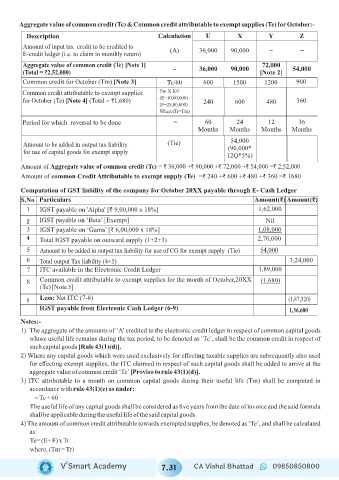

Aggregate value of common credit (Tc) & Common credit attributable to exempt supplies (Te) for October:-

Description Calculation U X Y Z

Amount of input tax credit to be credited to (A) 36,000 90,000 - -

E-credit ledger (i.e. to claim in monthly return)

Aggregate value of common credit (Tc) [Note 1] - 72,000

(Total = `2,52,000) 36,000 90,000 [Note 2] 54,000

Common credit for October (Tm) [Note 3] Tc/60 600 1500 1200 900

Common credit attributable to exempt supplies Tm X E/F

(E=10,00,000)

for October (Te) [Note 4] (Total = `1,680) 240 600 480 360

(F=25,00,000)

Where(Tr=Tm)

Period for which reversal to be done - 60 24 12 36

Months Months Months Months

54,000

Amount to be added in output tax liability (Tie) (90,000*

for use of capital goods for exempt supply

12Q*5%)

Amount of Aggregate value of common credit (Tc) = ` 36,000 +` 90,000 +` 72,000 +` 54,000 =` 2,52,000

Amount of common Credit Attributable to exempt supply (Te) =` 240 +` 600 +` 480 +` 360 =` 1680

Computation of GST liability of the company for October 20XX payable through E- Cash Ledger

S.No Particulars Amount(₹) Amount(₹)

1 IGST payable on 'Alpha' [` 9,00,000 x 18%] 1,62,000

2 IGST payable on ‘Beta’ [Exempt] Nil

3 IGST payable on ‘Gama’ [₹ 6,00,000 x 18%] 1,08,000

4 Total IGST payable on outward supply (1+2+3) 2,70,000

5 Amount to be added in output tax liability for use of CG for exempt supply (Tie) 54,000

6 Total output Tax liability (4+5) 3,24,000

7 ITC available in the Electronic Credit Ledger 1,89,000

8 Common credit attributable to exempt supplies for the month of October,20XX (1,680)

(Te) [Note 5]

9 Less: Net ITC (7-8) (1,87,320)

IGST payable from Electronic Cash Ledger (6-9) 1,36,680

Notes:-

1) The aggregate of the amounts of ‘A’ credited to the electronic credit ledger in respect of common capital goods

whose useful life remains during the tax period, to be denoted as ‘Tc’, shall be the common credit in respect of

such capital goods [Rule 43(1)(d)].

2) Where any capital goods which were used exclusively for effecting taxable supplies are subsequently also used

for effecting exempt supplies, the ITC claimed in respect of such capital goods shall be added to arrive at the

aggregate value of common credit ‘Tc’ [Proviso to rule 43(1)(d)].

3) ITC attributable to a month on common capital goods during their useful life (Tm) shall be computed in

accordance with rule 43(1)(e) as under:

= Tc ÷ 60

The useful life of any capital goods shall be considered as five years from the date of invoice and the said formula

shall be applicable during the useful life of the said capital goods

4) The amount of common credit attributable towards exempted supplies, be denoted as ‘Te’, and shall be calculated

as:

Te= (E÷ F) x Tr

where, (Tm = Tr)

V’Smart Academy 7.31 CA Vishal Bhattad 09850850800