Page 34 - Chap7 ITC

P. 34

‘E’ is the aggregate value of exempt supplies, made, during the tax period, and

‘F’ is the total turnover in the State of the registered person during the tax period [Rule 43(1)(g)].

Turnover of exempt supplies during the month of October

= Tm X

Total turnover of XYZ Pvt. Ltd. during the month of October

5) Common credit attributable to the exempt supplies (Te) along with the applicable interest (which is to be ignored

in this case) shall, during every tax period of the useful life of the concerned capital goods, be added to the

output tax liability of the person making such claim of credit [Rule 43(1)(h)].

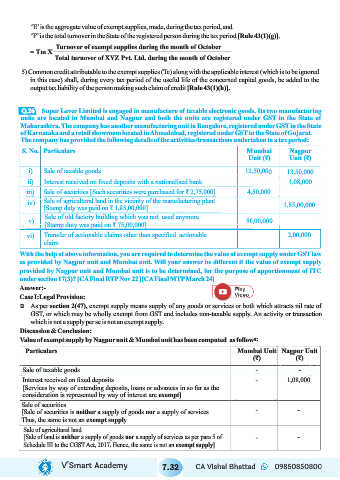

Super Lever Limited is engaged in manufacture of taxable electronic goods. Its two manufacturing

Q.26

units are located in Mumbai and Nagpur and both the units are registered under GST in the State of

Maharashtra. The company has another manufacturing unit in Bangalore, registered under GST in the State

of Karnataka and a retail showroom located in Ahmedabad, registered under GST in the State of Gujarat.

The company has provided the following details of the activities/transactions undertaken in a tax period:

S. No. Particulars Mumbai Nagpur

Unit (₹) Unit (₹)

i) Sale of taxable goods 12,50,000 13,50,000

ii) Interest received on fixed deposits with a nationalised bank 1,08,000

iii) Sale of securities [Such securities were purchased for ₹ 2,75,000] 4,50,000

iv) Sale of agricultural land in the vicinity of the manufacturing plant 1,85,00,000

[Stamp duty was paid on ₹ 1,85,00,000]

Sale of old factory building which was not used anymore

v) 90,00,000

[Stamp duty was paid on ₹ 75,00,000]

vi) Transfer of actionable claims other than specified actionable 2,00,000

claim

With the help of above information, you are required to determine the value of exempt supply under GST law

as provided by Nagpur unit and Mumbai unit. Will your answer be different if the value of exempt supply

provided by Nagpur unit and Mumbai unit is to be determined, for the purpose of apportionment of ITC

under section 17(3)? [CA Final RTP Nov 22 ][CA Final MTP March 24]

Answer:-

Case I:Legal Provision:

Ü As per section 2(47), exempt supply means supply of any goods or services or both which attracts nil rate of

GST, or which may be wholly exempt from GST and includes non-taxable supply. An activity or transaction

which is not a supply per se is not an exempt supply.

Discussion & Conclusion:

Value of exempt supply by Nagpur unit & Mumbai unit has been computed as follows:

Particulars Mumbai Unit Nagpur Unit

(₹) (₹)

Sale of taxable goods - -

Interest received on fixed deposits - 1,08,000

[Services by way of extending deposits, loans or advances in so far as the

consideration is represented by way of interest are exempt]

Sale of securities

- -

[Sale of securities is neither a supply of goods nor a supply of services.

Thus, the same is not an exempt supply

Sale of agricultural land

[Sale of land is neither a supply of goods nor a supply of services as per para 5 of - -

Schedule III to the CGST Act, 2017. Hence, the same is not an exempt supply]

V’Smart Academy 7.32 CA Vishal Bhattad 09850850800