Page 35 - Chap7 ITC

P. 35

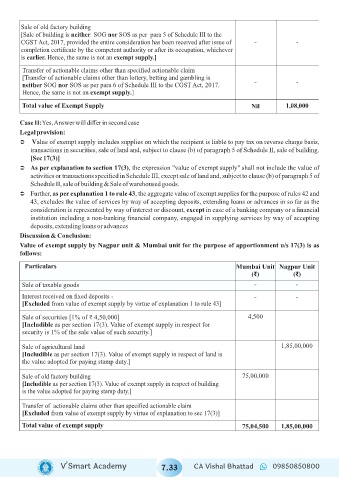

Sale of old factory building

[Sale of building is neither SOG nor SOS as per para 5 of Schedule III to the

CGST Act, 2017, provided the entire consideration has been received after issue of - -

completion certificate by the competent authority or after its occupation, whichever

is earlier. Hence, the same is not an exempt supply.]

Transfer of actionable claims other than specified actionable claim

[Transfer of actionable claims other than lottery, betting and gambling is

- -

neither SOG nor SOS as per para 6 of Schedule III to the CGST Act, 2017.

Hence, the same is not an exempt supply.]

Total value of Exempt Supply Nil 1,08,000

Case II:Yes, Answer will differ in second case

Legal provision:

Ü Value of exempt supply includes supplies on which the recipient is liable to pay tax on reverse charge basis,

transactions in securities, sale of land and, subject to clause (b) of paragraph 5 of Schedule II, sale of building.

[Sec 17(3)]

Ü As per explanation to section 17(3), the expression "value of exempt supply" shall not include the value of

activities or transactions specified in Schedule III, except sale of land and, subject to clause (b) of paragraph 5 of

Schedule II, sale of building & Sale of warehoused goods.

Ü Further, as per explanation 1 to rule 43, the aggregate value of exempt supplies for the purpose of rules 42 and

43, excludes the value of services by way of accepting deposits, extending loans or advances in so far as the

consideration is represented by way of interest or discount, except in case of a banking company or a financial

institution including a non-banking financial company, engaged in supplying services by way of accepting

deposits, extending loans or advances

Discussion & Conclusion:

Value of exempt supply by Nagpur unit & Mumbai unit for the purpose of apportionment u/s 17(3) is as

follows:

Particulars Mumbai Unit Nagpur Unit

(₹) (₹)

Sale of taxable goods - -

Interest received on fixed deposits - - -

[Excluded from value of exempt supply by virtue of explanation 1 to rule 43]

Sale of securities [1% of ₹ 4,50,000] 4,500

[Includible as per section 17(3). Value of exempt supply in respect for

security is 1% of the sale value of such security.]

Sale of agricultural land 1,85,00,000

[Includible as per section 17(3). Value of exempt supply in respect of land is

the value adopted for paying stamp duty.]

Sale of old factory building 75,00,000

[Includible as per section 17(3). Value of exempt supply in respect of building

is the value adopted for paying stamp duty.]

Transfer of actionable claims other than specified actionable claim

[Excluded from value of exempt supply by virtue of explanation to sec 17(3)]

Total value of exempt supply 75,04,500 1,85,00,000

V’Smart Academy 7.33 CA Vishal Bhattad 09850850800