Page 36 - Chap7 ITC

P. 36

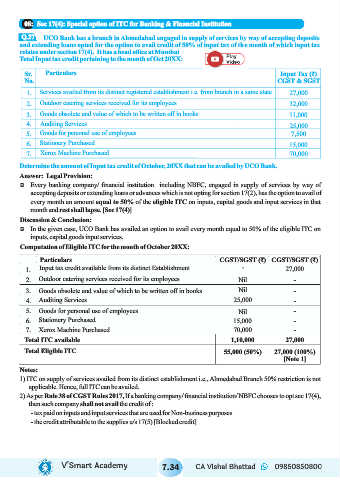

08: Sec 17(4): Special option of ITC for Banking & Financial Institution

Q.27

UCO Bank has a branch in Ahmedabad engaged in supply of services by way of accepting deposits

and extending loans opted for the option to avail credit of 50% of input tax of the month of which input tax

relates under section 17(4). It has a head office at Mumbai

Total Input tax credit pertaining to the month of Oct 20XX:

Sr. Particulars Input Tax (₹)

No. CGST & SGST

1. Services availed from its distinct registered establishment i.e. from branch in a same state 27,000

2. Outdoor catering services received for its employees 32,000

3. Goods obsolete and value of which to be written off in books 11,000

4. Auditing Services 25,000

5. Goods for personal use of employees 7,500

6. Stationery Purchased 15,000

7. Xerox Machine Purchased 70,000

Determine the amount of Input tax credit of October, 20XX that can be availed by UCO Bank.

Answer: Legal Provision:

Ü Every banking company/ financial institution including NBFC, engaged in supply of services by way of

accepting deposits or extending loans or advances which is not opting for section 17(2), has the option to avail of

every month an amount equal to 50% of the eligible ITC on inputs, capital goods and input services in that

month and rest shall lapse. [Sec 17(4)]

Discussion & Conclusion:

Ü In the given case, UCO Bank has availed an option to avail every month equal to 50% of the eligible ITC on

inputs, capital goods input services.

Computation of Eligible ITC for the month of October 20XX:

Particulars CGST/SGST (₹) CGST/SGST (₹)

1. Input tax credit available from its distinct Establishment - 27,000

2. Outdoor catering services received for its employees Nil -

3. Goods obsolete and value of which to be written off in books Nil -

4. Auditing Services 25,000 -

5. Goods for personal use of employees Nil -

6. Stationery Purchased 15,000 -

7. Xerox Machine Purchased 70,000 -

Total ITC available 1,10,000 27,000

Total Eligible ITC 55,000 (50%) 27,000 (100%)

[Note 1]

Notes:

1) ITC on supply of services availed from its distinct establishment i.e., Ahmedabad Branch 50% restriction is not

applicable. Hence, full ITC can be availed.

2) As per Rule 38 of CGST Rules 2017, If a banking company/ financial institution/ NBFC chooses to opt sec 17(4),

then such company shall not avail the credit of :

- tax paid on inputs and input services that are used for Non-business purposes

- the credit attributable to the supplies u/s 17(5) [Blocked credit]

V’Smart Academy 7.34 CA Vishal Bhattad 09850850800