Page 37 - Chap7 ITC

P. 37

09: Sec 18(1): Availability of Credit in Special Circumstances-

Q.28

Quanto Enterprises is not required to register under CGST Act. However, it applied for voluntary

registration on 17th September. Registration certificate has been granted to the firm on 25th September.

The CGST and SGST liability of the firm for the month of September is ₹ 24,000 each. The firm is not engaged

in making inter-State outward taxable supplies.

Quanto Enterprises provides the following information regarding capital goods and inputs held in stock by it

as on 24th September:

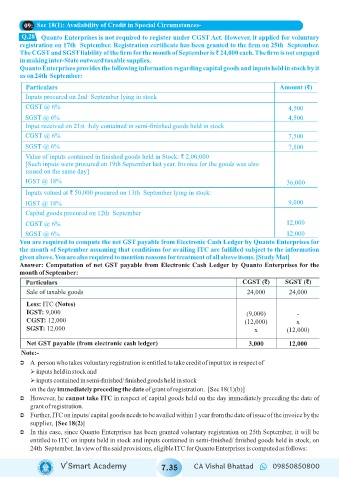

Particulars Amount (₹)

Inputs procured on 2nd September lying in stock

CGST @ 6% 4,500

SGST @ 6% 4,500

Input received on 21st July contained in semi-finished goods held in stock

CGST @ 6% 7,500

SGST @ 6% 7,500

Value of inputs contained in finished goods held in Stock: ₹ 2,00,000

[Such inputs were procured on 19th September last year. Invoice for the goods was also

issued on the same day]

IGST @ 18% 36,000

Inputs valued at ₹ 50,000 procured on 13th September lying in stock:

IGST @ 18% 9,000

Capital goods procured on 12th September

CGST @ 6% 12,000

SGST @ 6% 12,000

You are required to compute the net GST payable from Electronic Cash Ledger by Quanto Enterprises for

the month of September assuming that conditions for availing ITC are fulfilled subject to the information

given above. You are also required to mention reasons for treatment of all above items. [Study Mat]

Answer: Computation of net GST payable from Electronic Cash Ledger by Quanto Enterprises for the

month of September:

Particulars CGST (₹) SGST (₹)

Sale of taxable goods 24,000 24,000

Less: ITC (Notes)

IGST: 9,000 (9,000) -

CGST: 12,000 (12,000) x

SGST: 12,000 x (12,000)

Net GST payable (from electronic cash ledger) 3,000 12,000

Note:-

Ü A person who takes voluntary registration is entitled to take credit of input tax in respect of

Ø inputs held in stock and

Ø inputs contained in semi-finished/ finished goods held in stock

on the day immediately preceding the date of grant of registration. [Sec 18(1)(b)]

Ü However, he cannot take ITC in respect of capital goods held on the day immediately preceding the date of

grant of registration.

Ü Further, ITC on inputs/ capital goods needs to be availed within 1 year from the date of issue of the invoice by the

supplier, [Sec 18(2)]

Ü In this case, since Quanto Enterprises has been granted voluntary registration on 25th September, it will be

entitled to ITC on inputs held in stock and inputs contained in semi-finished/ finished goods held in stock, on

24th September. In view of the said provisions, eligible ITC for Quanto Enterprises is computed as follows:

V’Smart Academy 7.35 CA Vishal Bhattad 09850850800