Page 41 - Chap7 ITC

P. 41

3. The amount of the credit distributed shall not exceed the amount of credit available for distribution.

The credit related to an input service must be distributed only to the particular recipient to whom that

4.

input service is attributable.

If the input service is attributable to more than one recipient, the relevant ITC is distributed pro

5.

rata to such recipients in the ratio of turnover of the recipient in a State/ Union Territory to the

aggregate turnover of all the recipients to whom the input service is attributable and which are

operational during the current year.

6. ITC pertaining to input services which are common for all units, is distributed to all the recipients

in the ratio of turnover in the prescribed manner.

7. ITC available for distribution in a month shall be distributed in the same month and the details

thereof shall be furnished in the prescribed form.

8. Both ineligible and eligible ITC are to be distributed separately.

9. ITC of CGST, SGST/UTGST and IGST are to be distributed separately.

10. ITC of CGST, SGST/UTGST in respect of recipient located in the same State/Union Territory is

distributed as CGST and SGST/UTGST respectively.

11. ITC of CGST and SGST/UTGST, in respect of a recipient located in a different State/Union territory,

is distributed as IGST (total of ITC of CGST and SGST/UTGST which were to be distributed to such

recipient).

12. ITC on account of IGST is distributed as IGST.

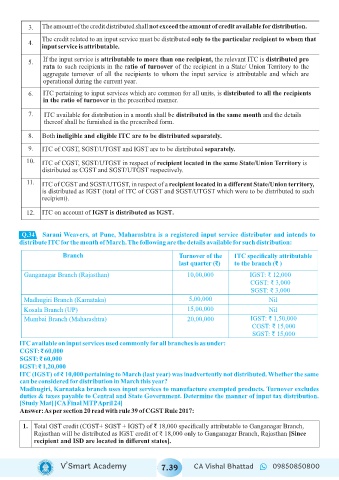

Q.34

Sarani Weavers, at Pune, Maharashtra is a registered input service distributor and intends to

distribute ITC for the month of March. The following are the details available for such distribution:

Branch Turnover of the ITC specifically attributable

last quarter (₹) to the branch (₹ )

Ganganagar Branch (Rajasthan) 10,00,000 IGST: ₹ 12,000

CGST: ₹ 3,000

SGST: ₹ 3,000

Madhugiri Branch (Karnataka) 5,00,000 Nil

Kosala Branch (UP) 15,00,000 Nil

Mumbai Branch (Maharashtra) 20,00,000 IGST: ₹ 1,50,000

CGST: ₹ 15,000

SGST: ₹ 15,000

lTC available on input services used commonly for all branches is as under:

CGST: ₹ 60,000

SGST: ₹ 60,000

IGST: ₹ 1,20,000

lTC (IGST) of ₹ 10,000 pertaining to March (last year) was inadvertently not distributed. Whether the same

can be considered for distribution in March this year?

Madhugiri, Karnataka branch uses input services to manufacture exempted products. Turnover excludes

duties & taxes payable to Central and State Government. Determine the manner of input tax distribution.

[Study Mat] [CA Final MTP April 24]

Answer: As per section 20 read with rule 39 of CGST Rule 2017:

1. Total GST credit (CGST+ SGST + IGST) of ₹ 18,000 specifically attributable to Ganganagar Branch,

Rajasthan will be distributed as IGST credit of ₹ 18,000 only to Ganganagar Branch, Rajasthan [Since

recipient and ISD are located in different states].

V’Smart Academy 7.39 CA Vishal Bhattad 09850850800