Page 11 - Chapter 10 Registration

P. 11

engaged in supply of produce out of cultivation of land. CCP 10.03.13.00

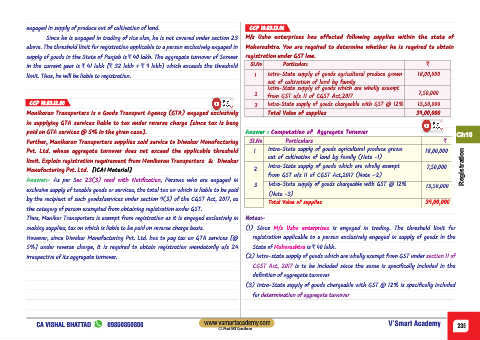

Since he is engaged in trading of rice also, he is not covered under section 23 M/s Usha enterprises has effected following supplies within the state of

above. The threshold limit for registration applicable to a person exclusively engaged in Maharashtra. You are required to determine whether he is required to obtain

supply of goods in the State of Punjab is ` 40 lakh. The aggregate turnover of Sameer registration under GST law.

in the current year is ` 41 lakh [` 32 lakh + ` 9 lakh] which exceeds the threshold SI.No Particulars `

limit. Thus, he will be liable to registration. 1 Intra-State supply of goods agricultural produce grown 18,00,000

out of cultivation of land by family

Intra-State supply of goods which are wholly exempt

2 7,50,000

from GST u/s 11 of CGST Act,2017

CCP 10.03.12.00

3 Intra-State supply of goods chargeable with GST @ 12% 13,50,000

Manikaran Transporters is a Goods Transport Agency (GTA) engaged exclusively Total Value of supplies 39,00,000

in supplying GTA services liable to tax under reverse charge [since tax is beng

paid on GTA services @ 5% in the given case]. Answer : Computation of Aggregate Turnover

Ch10

Further, Manikaran Transporters supplies said service to Diwakar Manufacturing SI.No Particulars `

Pvt. Ltd. whose aggregate turnover does not exceed the applicable threshold 1 Intra-State supply of goods agricultural produce grown 18,00,000

out of cultivation of land by family (Note -1)

limit. Explain registration requirement from Manikaran Transporters & Diwakar

Intra-State supply of goods which are wholly exempt 7,50,000 Registration

2

Manufacturing Pvt. Ltd. [ICAI Material]

from GST u/s 11 of CGST Act,2017 (Note –2)

Answer:- As per Sec 23(3) read with Notification , Persons who are engaged in

3 Intra-State supply of goods chargeable with GST @ 12% 13,50,000

exclusive supply of taxable goods or services, the total tax on which is liable to be paid

(Note -3)

by the recipient of such goods/services under section 9(3) of the CGST Act, 2017, as

Total Value of supplies 39,00,000

the category of person exempted from obtaining registration under GST.

Thus, Manikar Transporters is exempt from registration as it is engaged exclusively in Notes:-

making supplies, tax on which is liable to be paid on reverse charge basis. (1) Since M/s Usha enterprises is engaged in trading. The threshold limit for

However, since Diwakar Manufacturing Pvt. Ltd. has to pay tax on GTA services [@ registration applicable to a person exclusively engaged in supply of goods in the

5%] under reverse charge, it is required to obtain registration mandatorily u/s 24 State of Maharashtra is ` 40 lakh.

irrespective of its aggregate turnover. (2) Intra-state supply of goods which are wholly exempt from GST under section 11 of

CGST Act, 2017 is to be included since the same is specifically included in the

definition of aggregate turnover

(3) Intra-State supply of goods chargeable with GST @ 12% is specifically included

for determination of aggregate turnover

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 235

CA Final GST Questioner