Page 11 - 10. COMPILER QB - INDAS 36

P. 11

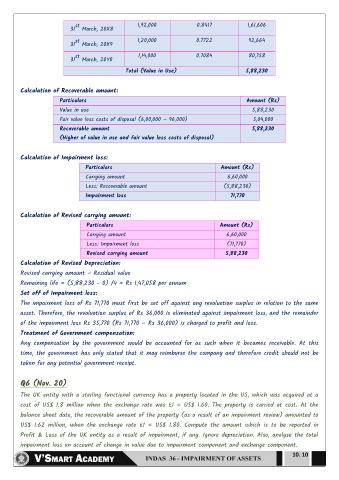

st 1,92,000 0.8417 1,61,606

31 March, 20X8

st 1,20,000 0.7722 92,664

31 March, 20X9

st 1,14,000 0.7084 80,758

31 March, 20Y0

Total (Value in Use) 5,88,230

Calculation of Recoverable amount:

Particulars Amount (Rs)

Value in use 5,88,230

Fair value less costs of disposal (6,00,000 – 96,000) 5,04,000

Recoverable amount 5,88,230

(Higher of value in use and fair value less costs of disposal)

Calculation of Impairment loss:

Particulars Amount (Rs)

Carrying amount 6,60,000

Less: Recoverable amount (5,88,230)

Impairment loss 71,770

Calculation of Revised carrying amount:

Particulars Amount (Rs)

Carrying amount 6,60,000

Less: Impairment loss (71,770)

Revised carrying amount 5,88,230

Calculation of Revised Depreciation:

Revised carrying amount – Residual value

Remaining life = (5,88,230 - 0) /4 = Rs 1,47,058 per annum

Set off of Impairment loss:

The impairment loss of Rs 71,770 must first be set off against any revaluation surplus in relation to the same

asset. Therefore, the revaluation surplus of Rs 36,000 is eliminated against impairment loss, and the remainder

of the impairment loss Rs 35,770 (Rs 71,770 – Rs 36,000) is charged to profit and loss.

Treatment of Government compensation:

Any compensation by the government would be accounted for as such when it becomes receivable. At this

time, the government has only stated that it may reimburse the company and therefore credit should not be

taken for any potential government receipt.

Q6 (Nov. 20)

The UK entity with a sterling functional currency has a property located in the US, which was acquired at a

cost of US$ 1.8 million when the exchange rate was ₤1 = US$ 1.60. The property is carried at cost. At the

balance sheet date, the recoverable amount of the property (as a result of an impairment review) amounted to

US$ 1.62 million, when the exchange rate ₤1 = US$ 1.80. Compute the amount which is to be reported in

Profit & Loss of the UK entity as a result of impairment, if any. Ignore depreciation. Also, analyse the total

impairment loss on account of change in value due to impairment component and exchange component.

10. 10