Page 12 - 3. COMPILER QB - INDAS 16

P. 12

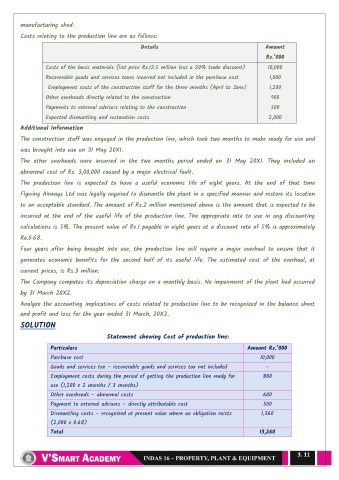

manufacturing shed.

Costs relating to the production line are as follows:

Details Amount

Rs.’000

Costs of the basic materials (list price Rs.12.5 million less a 20% trade discount) 10,000

Recoverable goods and services taxes incurred not included in the purchase cost 1,000

Employment costs of the construction staff for the three months (April to June) 1,200

Other overheads directly related to the construction 900

Payments to external advisors relating to the construction 500

Expected dismantling and restoration costs 2,000

Additional Information

The construction staff was engaged in the production line, which took two months to make ready for use and

was brought into use on 31 May 20X1.

The other overheads were incurred in the two months period ended on 31 May 20X1. They included an

abnormal cost of Rs. 3,00,000 caused by a major electrical fault.

The production line is expected to have a useful economic life of eight years. At the end of that time

Flywing Airways Ltd was legally required to dismantle the plant in a specified manner and restore its location

to an acceptable standard. The amount of Rs.2 million mentioned above is the amount that is expected to be

incurred at the end of the useful life of the production line. The appropriate rate to use in any discounting

calculations is 5%. The present value of Re.1 payable in eight years at a discount rate of 5% is approximately

Re.0·68.

Four years after being brought into use, the production line will require a major overhaul to ensure that it

generates economic benefits for the second half of its useful life. The estimated cost of the overhaul, at

current prices, is Rs.3 million.

The Company computes its depreciation charge on a monthly basis. No impairment of the plant had occurred

by 31 March 20X2.

Analyze the accounting implications of costs related to production line to be recognized in the balance sheet

and profit and loss for the year ended 31 March, 20X2.

SOLUTION

Statement showing Cost of production line:

Particulars Amount Rs.’000

Purchase cost 10,000

Goods and services tax – recoverable goods and services tax not included -

Employment costs during the period of getting the production line ready for 800

use (1,200 x 2 months / 3 months)

Other overheads – abnormal costs 600

Payment to external advisors – directly attributable cost 500

Dismantling costs – recognized at present value where an obligation exists 1,360

(2,000 x 0.68)

Total 13,260

3. 11