Page 9 - 3. COMPILER QB - INDAS 16

P. 9

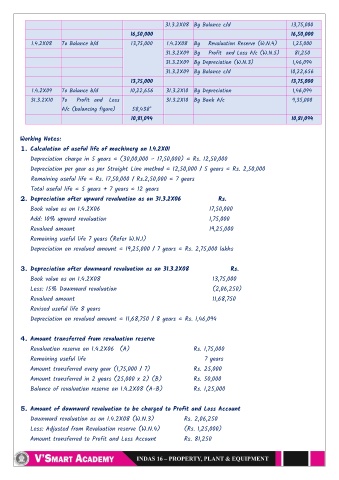

31.3.2X08 By Balance c/d 13,75,000

16,50,000 16,50,000

1.4.2X08 To Balance b/d 13,75,000 1.4.2X08 By Revaluation Reserve (W.N.4) 1,25,000

31.3.2X09 By Profit and Loss A/c (W.N.5) 81,250

31.3.2X09 By Depreciation (W.N.3) 1,46,094

31.3.2X09 By Balance c/d 10,22,656

13,75,000 13,75,000

1.4.2X09 To Balance b/d 10,22,656 31.3.2X10 By Depreciation 1,46,094

31.3.2X10 To Profit and Loss 31.3.2X10 By Bank A/c 9,35,000

A/c (balancing figure) 58,438*

10,81,094 10,81,094

Working Notes:

1. Calculation of useful life of machinery on 1.4.2X01

Depreciation charge in 5 years = (30,00,000 – 17,50,000) = Rs. 12,50,000

Depreciation per year as per Straight Line method = 12,50,000 / 5 years = Rs. 2,50,000

Remaining useful life = Rs. 17,50,000 / Rs.2,50,000 = 7 years

Total useful life = 5 years + 7 years = 12 years

2. Depreciation after upward revaluation as on 31.3.2X06 Rs.

Book value as on 1.4.2X06 17,50,000

Add: 10% upward revaluation 1,75,000

Revalued amount 19,25,000

Remaining useful life 7 years (Refer W.N.1)

Depreciation on revalued amount = 19,25,000 / 7 years = Rs. 2,75,000 lakhs

3. Depreciation after downward revaluation as on 31.3.2X08 Rs.

Book value as on 1.4.2X08 13,75,000

Less: 15% Downward revaluation (2,06,250)

Revalued amount 11,68,750

Revised useful life 8 years

Depreciation on revalued amount = 11,68,750 / 8 years = Rs. 1,46,094

4. Amount transferred from revaluation reserve

Revaluation reserve on 1.4.2X06 (A) Rs. 1,75,000

Remaining useful life 7 years

Amount transferred every year (1,75,000 / 7) Rs. 25,000

Amount transferred in 2 years (25,000 x 2) (B) Rs. 50,000

Balance of revaluation reserve on 1.4.2X08 (A-B) Rs. 1,25,000

5. Amount of downward revaluation to be charged to Profit and Loss Account

Downward revaluation as on 1.4.2X08 (W.N.3) Rs. 2,06,250

Less: Adjusted from Revaluation reserve (W.N.4) (Rs. 1,25,000)

Amount transferred to Profit and Loss Account Rs. 81,250

3.8