Page 8 - 3. COMPILER QB - INDAS 16

P. 8

nature and use of land operated as a landfill site is different from vacant land. Hence, the entity should disclose

Property A separately. The entity must apply judgment to determine whether the entity‖s retail outlets are

sufficiently different in nature and use from its office buildings, and thus constitute a separate class of land

and buildings.

The computer equipment is integrated across the organisation and would probably be classified as a single

separate class of asset.

Furniture and fittings used for administrative purposes could be sufficiently different to shop fixtures and

fittings in retail outlets. Hence, they should be classified in two separate classes of assets.

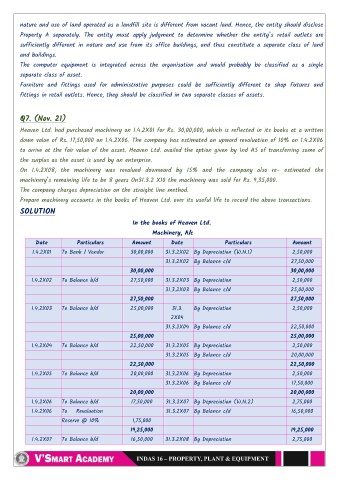

Q7. (Nov. 21)

Heaven Ltd. had purchased machinery on 1.4.2X01 for Rs. 30,00,000, which is reflected in its books at a written

down value of Rs. 17,50,000 on 1.4.2X06. The company has estimated an upward revaluation of 10% on 1.4.2X06

to arrive at the fair value of the asset. Heaven Ltd. availed the option given by Ind AS of transferring some of

the surplus as the asset is used by an enterprise.

On 1.4.2X08, the machinery was revalued downward by 15% and the company also re- estimated the

machinery‖s remaining life to be 8 years On31.3.2 X10 the machinery was sold for Rs. 9,35,000.

The company charges depreciation on the straight line method.

Prepare machinery accounts in the books of Heaven Ltd. over its useful life to record the above transactions.

SOLUTION

In the books of Heaven Ltd.

Machinery, A/c

Date Particulars Amount Date Particulars Amount

1.4.2X01 To Bank / Vendor 30,00,000 31.3.2X02 By Depreciation (W.N.1) 2,50,000

31.3.2X02 By Balance c/d 27,50,000

30,00,000 30,00,000

1.4.2X02 To Balance b/d 27,50,000 31.3.2X03 By Depreciation 2,50,000

31.3.2X03 By Balance c/d 25,00,000

27,50,000 27,50,000

1.4.2X03 To Balance b/d 25,00,000 31.3. By Depreciation 2,50,000

2X04

31.3.2X04 By Balance c/d 22,50,000

25,00,000 25,00,000

1.4.2X04 To Balance b/d 22,50,000 31.3.2X05 By Depreciation 2,50,000

31.3.2X05 By Balance c/d 20,00,000

22,50,000 22,50,000

1.4.2X05 To Balance b/d 20,00,000 31.3.2X06 By Depreciation 2,50,000

31.3.2X06 By Balance c/d 17,50,000

20,00,000 20,00,000

1.4.2X06 To Balance b/d 17,50,000 31.3.2X07 By Depreciation (W.N.2) 2,75,000

1.4.2X06 To Revaluation 31.3.2X07 By Balance c/d 16,50,000

Reserve @ 10% 1,75,000

19,25,000 19,25,000

1.4.2X07 To Balance b/d 16,50,000 31.3.2X08 By Depreciation 2,75,000

3.7