Page 13 - 16. COMPILER QB - INDAS 103

P. 13

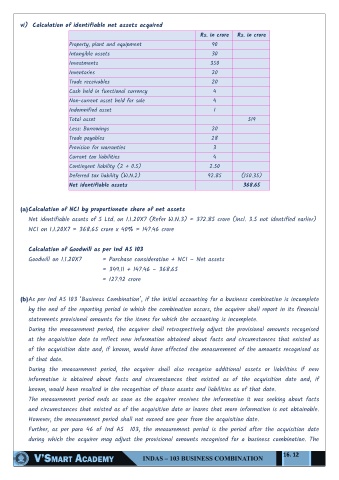

vi) Calculation of identifiable net assets acquired

Rs. in crore Rs. in crore

Property, plant and equipment 90

Intangible assets 30

Investments 350

Inventories 20

Trade receivables 20

Cash held in functional currency 4

Non-current asset held for sale 4

Indemnified asset 1

Total asset 519

Less: Borrowings 20

Trade payables 28

Provision for warranties 3

Current tax liabilities 4

Contingent liability (2 + 0.5) 2.50

Deferred tax liability (W.N.2) 92.85 (150.35)

Net identifiable assets 368.65

(a) Calculation of NCI by proportionate share of net assets

Net identifiable assets of S Ltd. on 1.1.20X7 (Refer W.N.3) = 372.85 crore (incl. 3.5 not identified earlier)

NCI on 1.1.20X7 = 368.65 crore x 40% = 147.46 crore

Calculation of Goodwill as per Ind AS 103

Goodwill on 1.1.20X7 = Purchase consideration + NCI – Net assets

= 349.11 + 147.46 – 368.65

= 127.92 crore

(b) As per Ind AS 103 ―Business Combination‖, if the initial accounting for a business combination is incomplete

by the end of the reporting period in which the combination occurs, the acquirer shall report in its financial

statements provisional amounts for the items for which the accounting is incomplete.

During the measurement period, the acquirer shall retrospectively adjust the provisional amounts recognised

at the acquisition date to reflect new information obtained about facts and circumstances that existed as

of the acquisition date and, if known, would have affected the measurement of the amounts recognised as

of that date.

During the measurement period, the acquirer shall also recognise additional assets or liabilities if new

information is obtained about facts and circumstances that existed as of the acquisition date and, if

known, would have resulted in the recognition of those assets and liabilities as of that date.

The measurement period ends as soon as the acquirer receives the information it was seeking about facts

and circumstances that existed as of the acquisition date or learns that more information is not obtainable.

However, the measurement period shall not exceed one year from the acquisition date.

Further, as per para 46 of Ind AS 103, the measurement period is the period after the acquisition date

during which the acquirer may adjust the provisional amounts recognised for a business combination. The

16. 12