Page 21 - 19. COMPILER QB - INDAS 115

P. 21

SOLUTION

Determining whether a good or service represents a performance obligation on its own or is required to be

aggregated with other goods or services can have a significant impact on the timing of revenue recognition.

While the customer may be able to benefit from each promised good or service on its own (or together with

other readily available resources), they do not appear to be separately identifiable within the context of the

contract. That is, the promised goods and services are subject to significant integration, and as a result will

be treated as a single performance obligation.

This is consistent with a view that the customer is primarily interested in acquiring a single asset (a water

purification plant) rather than a collection of related components and services.

Q20. (OCT 21)

Growth Ltd. enters into an arrangement with a customer for an infrastructure outsourcing deal.

Based on its experience, Growth Ltd. determines that customizing the infrastructure will take approximately

200 hours in total to complete the project and charges Rs. 150 per hour.

After incurring 100 hours of time, Growth Ltd. and the customer agree to change an aspect of the project and

increase the estimate of labour hours by 50 hours at the rate of Rs. 100 per hour.

Determine how contract modification will be accounted as per Ind AS 115?

SOLUTION

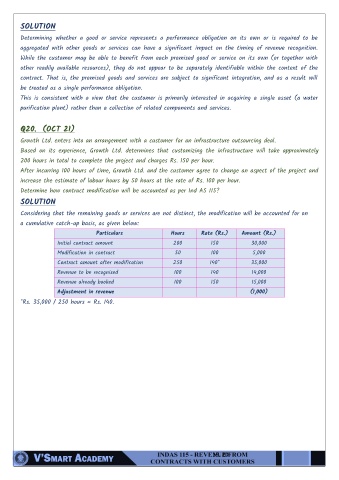

Considering that the remaining goods or services are not distinct, the modification will be accounted for on

a cumulative catch-up basis, as given below:

Particulars Hours Rate (Rs.) Amount (Rs.)

Initial contract amount 200 150 30,000

Modification in contract 50 100 5,000

Contract amount after modification 250 140* 35,000

Revenue to be recognised 100 140 14,000

Revenue already booked 100 150 15,000

Adjustment in revenue (1,000)

*Rs. 35,000 / 250 hours = Rs. 140.

19. 20