Page 9 - 23. COMPILER QB - IND AS 109_32

P. 9

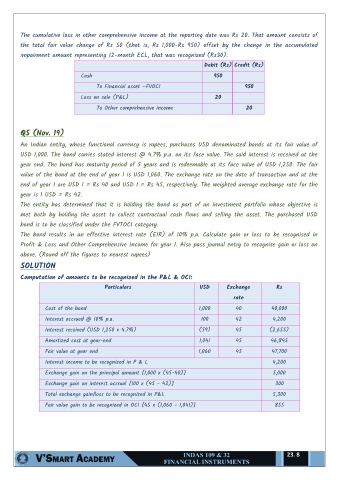

The cumulative loss in other comprehensive income at the reporting date was Rs 20. That amount consists of

the total fair value change of Rs 50 (that is, Rs 1,000-Rs 950) offset by the change in the accumulated

impairment amount representing 12-month ECL, that was recognized (Rs30).

Debit (Rs) Credit (Rs)

Cash 950

To Financial asset –FVOCI 950

Loss on sale (P&L) 20

To Other comprehensive income 20

Q5 (Nov. 19)

An Indian entity, whose functional currency is rupees, purchases USD denominated bonds at its fair value of

USD 1,000. The bond carries stated interest @ 4.7% p.a. on its face value. The said interest is received at the

year end. The bond has maturity period of 5 years and is redeemable at its face value of USD 1,250. The fair

value of the bond at the end of year 1 is USD 1,060. The exchange rate on the date of transaction and at the

end of year 1 are USD 1 = Rs 40 and USD 1 = Rs 45, respectively. The weighted average exchange rate for the

year is 1 USD = Rs 42.

The entity has determined that it is holding the bond as part of an investment portfolio whose objective is

met both by holding the asset to collect contractual cash flows and selling the asset. The purchased USD

bond is to be classified under the FVTOCI category.

The bond results in an effective interest rate (EIR) of 10% p.a. Calculate gain or loss to be recognised in

Profit & Loss and Other Comprehensive Income for year 1. Also pass journal entry to recognise gain or loss on

above. (Round off the figures to nearest rupees)

SOLUTION

Computation of amounts to be recognized in the P&L & OCI:

Particulars USD Exchange Rs

rate

Cost of the bond 1,000 40 40,000

Interest accrued @ 10% p.a. 100 42 4,200

Interest received (USD 1,250 x 4.7%) (59) 45 (2,655)

Amortized cost at year-end 1,041 45 46,845

Fair value at year end 1,060 45 47,700

Interest income to be recognized in P & L 4,200

Exchange gain on the principal amount [1,000 x (45-40)] 5,000

Exchange gain on interest accrual [100 x (45 - 42)] 300

Total exchange gain/loss to be recognized in P&L 5,300

Fair value gain to be recognized in OCI [45 x (1,060 - 1,041)] 855

23. 8