Page 19 - 30. COMPILER QB - IND AS 101

P. 19

is to be repaid in equal installments over the period of ten years at the year end. Interest is also

payable at each year end. The fair value of loan as on the date of transition is Rs 50,000 as against the

carrying amount of loan which at present amounts to Rs 40,000. However, Ind AS 109 mandates to

charge the interest expense as per effective interest method after the adjustment of transaction costs.

Management says it is a tedious task in the given case to apply the effective interest rate changes with

retrospective effect and hence is reluctant to apply the same retrospectively in its first-time adoption.

f) In the long-term borrowings, Rs 4,50,000 of component is due towards the State Government. Interest is

payable on the government loan at 4%, however the prevailing rate in the market at present is 8%. The

fair market value of the loan stands at Rs 4,20,000 as on the relevant date.

g) Under Previous GAAP, the mutual funds were measured at cost or market value, whichever is lower. Under

Ind AS, the Company has designated these investments at fair value through profit or loss. The value of

mutual funds as per previous GAAP is Rs 2,00,000 as included in ‘current investment’. However, the fair

value of mutual funds as on the date of transition is Rs 2,30,000.

h) Ignore separate calculation of deferred tax on above adjustments. Assume the net deferred tax income to

be Rs 50,000 on account of Ind AS transition adjustments.

Requirements:

- Prepare transition date balance sheet of Shaurya Limited as per Indian Accounting Standards

Show necessary explanation for each of the items presented by the chief financial officer in the form of

notes, which may or may not require the adjustment as on the date of transition.

SOLUTION

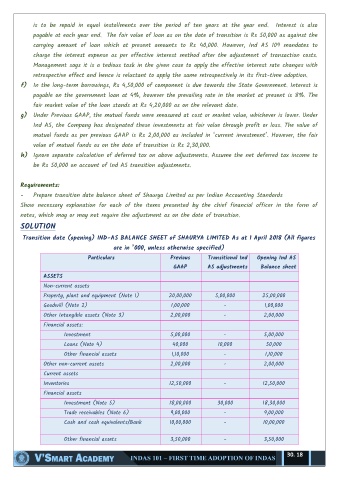

Transition date (opening) IND-AS BALANCE SHEET of SHAURYA LIMITED As at 1 April 2018 (All figures

are in ’000, unless otherwise specified)

Particulars Previous Transitional Ind Opening Ind AS

GAAP AS adjustments Balance sheet

ASSETS

Non-current assets

Property, plant and equipment (Note 1) 20,00,000 5,00,000 25,00,000

Goodwill (Note 2) 1,00,000 - 1,00,000

Other Intangible assets (Note 3) 2,00,000 - 2,00,000

Financial assets:

Investment 5,00,000 - 5,00,000

Loans (Note 4) 40,000 10,000 50,000

Other financial assets 1,10,000 - 1,10,000

Other non-current assets 2,00,000 - 2,00,000

Current assets

Inventories 12,50,000 - 12,50,000

Financial assets

Investment (Note 5) 18,00,000 30,000 18,30,000

Trade receivables (Note 6) 9,00,000 - 9,00,000

Cash and cash equivalents/Bank 10,00,000 - 10,00,000

Other financial assets 3,50,000 - 3,50,000

30. 18